As an entrepreneur, it’s important to consider how business structure can impact the taxation, legal protection, and growth potential of your company. S corp and C corp are two types of corporations that offer unique benefits and limitations.

S corporations offer pass-through taxation and asset protection, but come with ownership restrictions. C corporations provide multiple classes of stock options and employee benefits with potential tax deductions, but are subject to double taxation on corporate income. Ultimately, the choice will depend on your business’ size and long-term goals.

Key takeaways

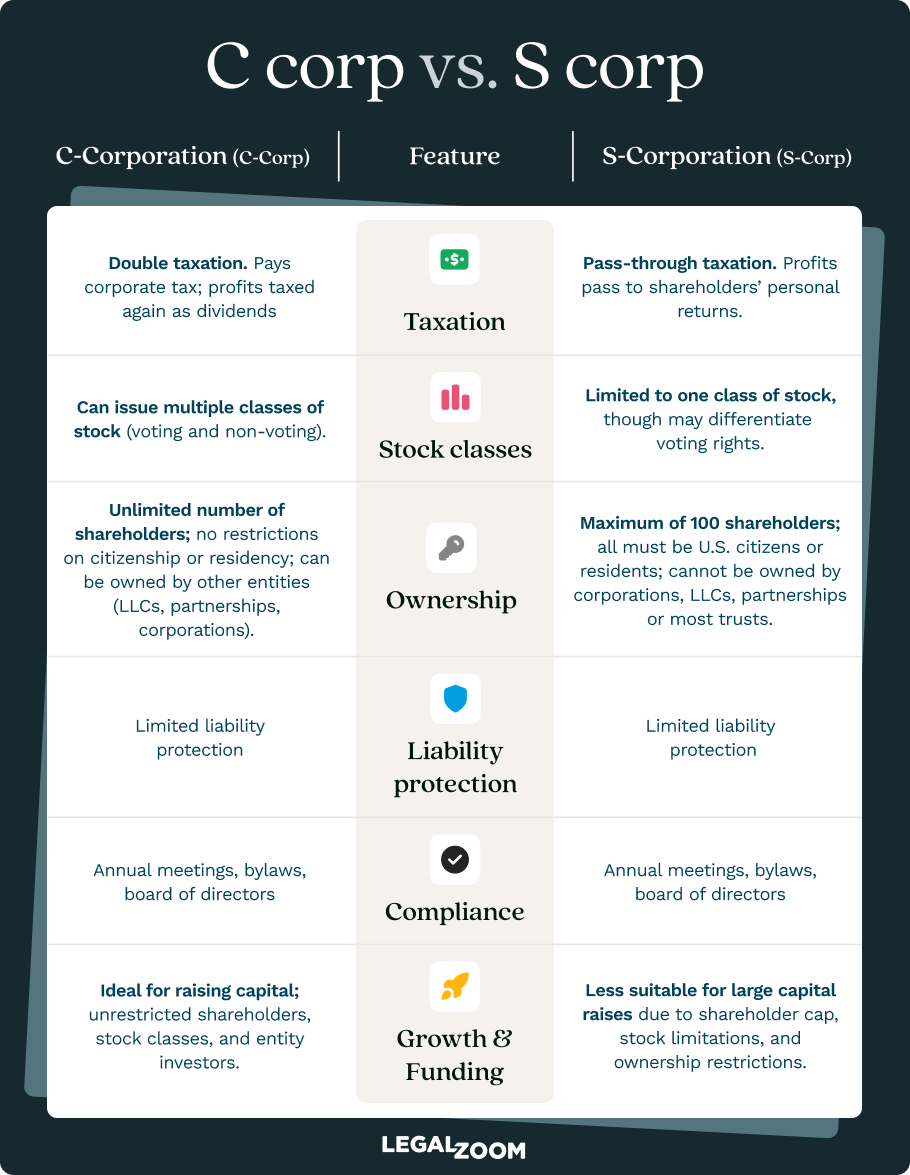

- Taxation. S corporations do not pay federal income tax at the entity level; instead, profits and losses pass through to shareholders, who report them on their individual tax returns. C corporations pay taxes at the corporate level.

- Ownership. S corporations can only have up to 100 shareholders and only one class of stock, which may limit its ability to raise funds and entice investors. C corporations can have unlimited shareholders and various types of stock.

- State regulations. States generally don’t distinguish between S and C corporations. That means that both business structures need to file articles of incorporation with the state to incorporate and need to stay up-to-date on corporate compliance issues.

- Formation. Once a corporation has registered with the state, it needs to file Form 2553 with the Internal Revenue Service (IRS) to gain S corporation status.

Defining S corporations and C corporations

S corporations and C corporations are two types of corporate structures that face different regulations under the Internal Revenue Code. S corporations get their name from Subchapter S of Chapter 1 of the Internal Revenue Code, which permits this type of legal entity.

S corporations

An S corporation is a corporation that elects to pass taxable income, losses, deductions, and credits through to its shareholders' personal tax returns. By transferring gains and losses to shareholders for federal income tax purposes, S corporations avoid double taxation on corporate income. To become an S corporation, businesses must file Form 2553 with the Internal Revenue Service after filing articles of incorporation with the relevant state.

Pass-through taxation provides various tax benefits for small businesses. Not only does this designation prevent shareholders from being taxed twice, but it can also help to lower self-employment taxes. For example, shareholders who are also employees receive a salary and may receive distributions. In this case, only the salary portion is subject to payroll taxes.

To qualify for S corporation status, the company must be domestic with no more than 100 shareholders and only one type of stock. The shareholders also need to be U.S. citizens or residents.

C corporations

C corporations are the default for all corporations. Every corporation is a C corp until it files Form 2553 and receives approval to become an S corp. Like S corporations, they’re independent legal entities that shareholders own. Unlike S corporations, they possess unlimited growth potential but are subject to double taxation.

Double taxation means that income is taxed in two ways: The corporation pays taxes on its profits at the corporate level, while shareholders pay federal taxes on dividends they receive from the corporation at the individual level.

Still, C corporations have benefits. They can issue multiple classes of stock and have no restrictions on how many shareholders there are, which gives them more flexibility in terms of ownership and stock options.

To form a C corporation, businesses must submit articles of incorporation to the Secretary of State (SOS) or similar agency that handles business filings in the state where they’ll operate.

Similarities between S corporations and C corporations

Although S and C corporations differ in several aspects, they share key similarities when it comes to liability protection, corporate governance, and legal requirements.

Limited liability protection safeguards the owners' personal assets from the claims of business creditors. In other words, shareholders of corporations are not personally financially liable for corporate debts, and creditors can’t use their personal assets to satisfy the business' debts.

Corporate governance involves a formal structure for managing and overseeing the company's operations. In both S corporations and C corporations, corporate governance typically includes the following features:

- Shareholders who have ownership in the company and may have voting rights and receive dividends

- A board of directors responsible for making major decisions and setting the strategic direction of the company

- Officers, such as the CEO, COO, and CFO, tasked with day-to-day operations and management

Legal requirements, such as compliance requirements, exist for both types of corporations. For example, they’re both mandated to comply with state and federal regulations, file annual reports, hold annual meetings, and pay fees and taxes.

Differences between S corporations and C corporations

Important differences between C and S corporations include their formation, taxation, ownership, stock practices, and employee benefits.

Formation. In the eyes of the IRS, all corporations automatically begin as C corporations when they form. A C corporation may convert to an S corp by filing IRS Form 2553, Election by a Small Business Corporation, with the IRS if it meets the eligibility requirements.

To obtain S corp status for a certain year, you must file Form 2553 by March 15 of that calendar year, or, for corporations operating on an alternative fiscal year, no later than the 15th day of the third month of that fiscal year.

Taxation. The main reason to choose an S corp is to save on taxes.

- C corporations report profits on the corporation's own tax return. After-tax profits then distribute to shareholders as dividends, where they face taxes again on shareholder’s personal tax returns. C corporations file taxes on Form 1120.

- S corporations file taxes like a sole proprietorship, LLC, or a partnership does. The business’ profits (or losses) pass through to the shareholders, who pay taxes and report them only once on their personal tax returns. S corporations file on Form 1120-S.

Many states also pass profits and losses through to the owners of S corporations. However, a few states unfortunately engage in double taxation of S corporations. This is a key factor to take into account as a business owner when deciding where you want to incorporate.

Ownership. A C corporation provides more flexibility in selling stock shares than an S corp. According to the IRS, a corporation that elects S corp status faces the following restrictions:

- No more than 100 shareholders

- No more than one class of stock

- Shareholders must be U.S. citizens or residents

- Shareholders can’t be a C corporation, other S corporation, LLC, partnership, or ineligible trust

Stocks and shares. C corporations place minimal limits on shareholders and issue multiple types of stock. For this reason, they’re more likely to appeal to investors, such as venture capital and private equity firms. Because they can issue more than one class of stock it may be easier for a C corp to raise capital from investors for growth without giving them voting rights.

Benefit deductions. Any company may choose to provide benefits to its shareholders, who are also its employees, such as health, life, and disability insurance. C corporations can deduct the cost of these benefits so they won't be taxable to the shareholder—as long as the benefits extend to at least 70% of the employees.

Conversely, S corporations face more restrictions on benefit deductions. For example, they can only deduct the cost of benefits that they pay on behalf of a shareholder who owns more than 2% of the company's stock.

Pros and cons of S corporations

S corporations offer certain advantages and disadvantages that small business owners should consider when evaluating and choosing a corporate structure.

Advantages of S corporations

- Avoids double taxation. S corp stats allows for pass-through taxation, which allows shareholders to report the corporation's income, losses, deductions, and credits on their individual tax returns.

- Limited liability protection. S corporations provide some asset protection to their shareholders by helping to shield shareholder's personal property from potential lawsuits or debt collections directed at the S corp.

- Streamlined process of transferring ownership shares. S corporation stock is generally transferable. This makes it easier to change ownership than in other business structures, which can be particularly beneficial for small businesses looking to expand and acquire new owners.

- Saves on self-employment taxes. S corp shareholders can reduce the portion of their earnings that are subject to FICA taxes by splitting wages and distributions. Essentially, by portioning part of their earnings off as salary wages and part as distributions, shareholders only pay self-employment taxes on the wage portion.

Disadvantages of S corporations

- Ownership restrictions. S corp status limits the number of shareholders to a maximum of 100 and requires all shareholders to be U.S. citizens or residents. Additionally, certain entities, such as other corporations and non-resident foreigners, aren’t eligible to own shares in an S corporation.

- Limited stock options. S corporations are restricted to having only one class of stock, which may impact the corporation's ability to raise capital, attract investors, and offer competitive employee benefits.

- Restricted benefit deductions. They face limitations on deductible benefits, such as high deductible health insurance premiums, wellness or preventive care, and health stipends for S corp shareholders.

Pros and cons of C corporations

C corporations have more ownership flexibility and stock options, despite their two levels of taxation, which may appeal more to entrepreneurs with high-growth expectations.

Advantages of C corporations

- Greater ownership flexibility. C corp can have an unlimited number of shareholders, with no restrictions on who or what can own shares. This flexibility allows C corporations to attract a broader range of investors to raise capital for the business

- Unlimited stock options. C corporations can issue multiple classes of stock and unlimited numbers of shares. More stock options means more options in terms of ownership, control, and voting rights.

- More employee benefit deductions. C corp status can provide tax deductions and tax-free fringe benefits for both the corporation and its shareholders or employees. This includes health insurance, retirement plans, and other perks that are fully deductible.

Disadvantages of C corporations

- Double taxation. C corporations are taxed on their corporate income profits at the corporate level and shareholders pay taxes on dividends. This can result in higher overall tax liabilities for both the corporation and its shareholders.

- More complex fling requirements. C corporations generally have more complex filing requirements than S corporations. Besides filing both corporate and personal tax returns, a C corp that goes public also needs to file annual SEC reports.

What to consider when choosing a corp type

- Pass-through tax benefits. An S corporation doesn’t pay corporate taxes at the federal level, while a C corporation does.

- Employee income. S corporation shareholders can work as employees of the corporation and receive a salary.

- Simple transfer of ownership. Shareholders can transfer their interest in an S corporation with little to no tax consequences.

- Single taxation level on business sales. When owners sell an S corporation, they only pay taxes on the distribution. With C corporations, the corporation pays taxes first, and shareholders pay taxes again once they receive their proceeds.

- Taxes on benefits. S corporations can only deduct corporate benefits, such as medical insurance, that they pay on behalf of shareholders who own more than 2% of the S corp.

- Stock restrictions. S corporations can only have 100 shareholders and only one class of stock, although they can issue both voting and non-voting shares.

- IRS scrutiny. The IRS scrutinizes S corp payments to ensure they reflect dividends and salaries accurately.

- Accidental termination. S corporations lose their tax status when shareholders transfer interest to restricted parties, such as a nonresident alien.

How to choose between an S corp and a C corp

Both S corporations and C corporations have their own unique advantages and disadvantages, and the ideal choice will depend on the specific needs and goals of the entrepreneur. Here are some factors to keep in mind when choosing between the two.

- Business size and goals. Generally, smaller businesses may prefer to set up as an S corp due to its pass-through taxation and ease of use. Larger businesses that hope to significantly expand and access external investors may opt for a C corp structure to take advantage of its ownership flexibility and ability to issue different classes of stock.

- Tax implications. When it comes to managing finances, business owners should carefully evaluate the tax consequences of each structure in relation to their specific financial situation and objectives.

- Acquisitions. It may be easier to sell a C corporation than an S corporation. C corporations face minimal restrictions on who can buy shares and when. On the other hand, S corporations allow for fewer shareholders, and investors must pay taxes on the income from their shares.

- IRS scrutiny. Because of their tax arrangement, the IRS keeps closer tabs on S corporations. To maintain S corp status, it’s critical to avoid mistakes and errors that could lead to audits.

FAQs

What are the exact IRS deadlines and procedures for filing Form 2553 to elect S corp status?

The deadline to file Form 2553 is March 15 for companies whose financial year aligns with the calendar year, or, the 15th day of the third month of their fiscal year for corporations that operate on an alternative financial year.

How does self-employment tax treatment differ between S corp shareholder-employees and sole proprietors?

S corporations can potentially minimize their self-employment taxes by reasonably distributing their earnings between salary and dividends. Sole proprietors, on the other hand, must pay self-employment taxes on all of their income.

What state-by-state variations exist in S corp taxation or eligibility?

S and C corporations are technically separate designations for corporations that the IRS recognizes for federal tax purposes. Not all states differentiate between S corp and C corp status. While some states that do recognize S corp status will allow those companies certain tax benefits, like “pass-through” taxation, other states treat all corporations as C corporations regardless of their IRS designation.

How do you convert an S corp back to a C corp, and what are the tax implications?

To convert a C corp into an S corp, you need to file Form 2553 with the IRS. However, only qualified small businesses with a limited number of shareholders and one class of stock can receive S corp status. Owners of S corporations can avoid paying taxes on the same income twice by reporting their gains and losses directly through their shareholders' personal income tax returns. This method is called “pass-through” taxation.

Can an S corp issue nonvoting shares, and how does that affect control and funding?

Yes, S corporations can issue both voting and nonvoting shares as long as they’re only one class of stock.

Brette Sember, J.D., contributed to this article.

'%20/%3e%3c/svg%3e)

'%3e%3cpath%20fill-rule='evenodd'%20clip-rule='evenodd'%20d='M9.31239%2025.5316H13.0679V14.1032H9.31239V25.5316ZM11.1913%208.46875C9.93945%208.46875%209%209.25086%209%2010.505C9%2011.5995%209.78211%2012.5389%2011.1913%2012.5389C12.6005%2012.5389%2013.3826%2011.5995%2013.3826%2010.505C13.3826%209.4082%2012.6005%208.46875%2011.1913%208.46875ZM27%2018.9577V25.5316H23.2445V19.4275C23.2445%2017.8609%2022.6174%2016.7664%2021.3679%2016.7664C20.2711%2016.7664%2019.644%2017.5463%2019.3316%2018.1756C19.1743%2018.488%2019.1743%2018.8004%2019.1743%2019.1128V25.5316H15.4165V13.9458H19.1743V15.5123C19.644%2014.7302%2020.5835%2013.6357%2022.6174%2013.6357C25.1234%2013.7908%2027%2015.3573%2027%2018.9577Z'%20fill='white'/%3e%3c/g%3e%3cdefs%3e%3cclipPath%20id='clip0_952_9489'%3e%3crect%20width='18'%20height='18'%20fill='white'%20transform='translate(9%208)'/%3e%3c/clipPath%3e%3c/defs%3e%3c/svg%3e)