S corporations have tax advantages that make them a good choice for many small businesses. An S corp is a tax designation that allows a company's profits to pass through to the owners' personal tax returns. Both corporations and limited liability companies (LLCs) can choose to be taxed as an S corp.

But there are also some disadvantages, and not every business is eligible to be an S corp. Read on to figure out if it's right for you.

What is an S corp?

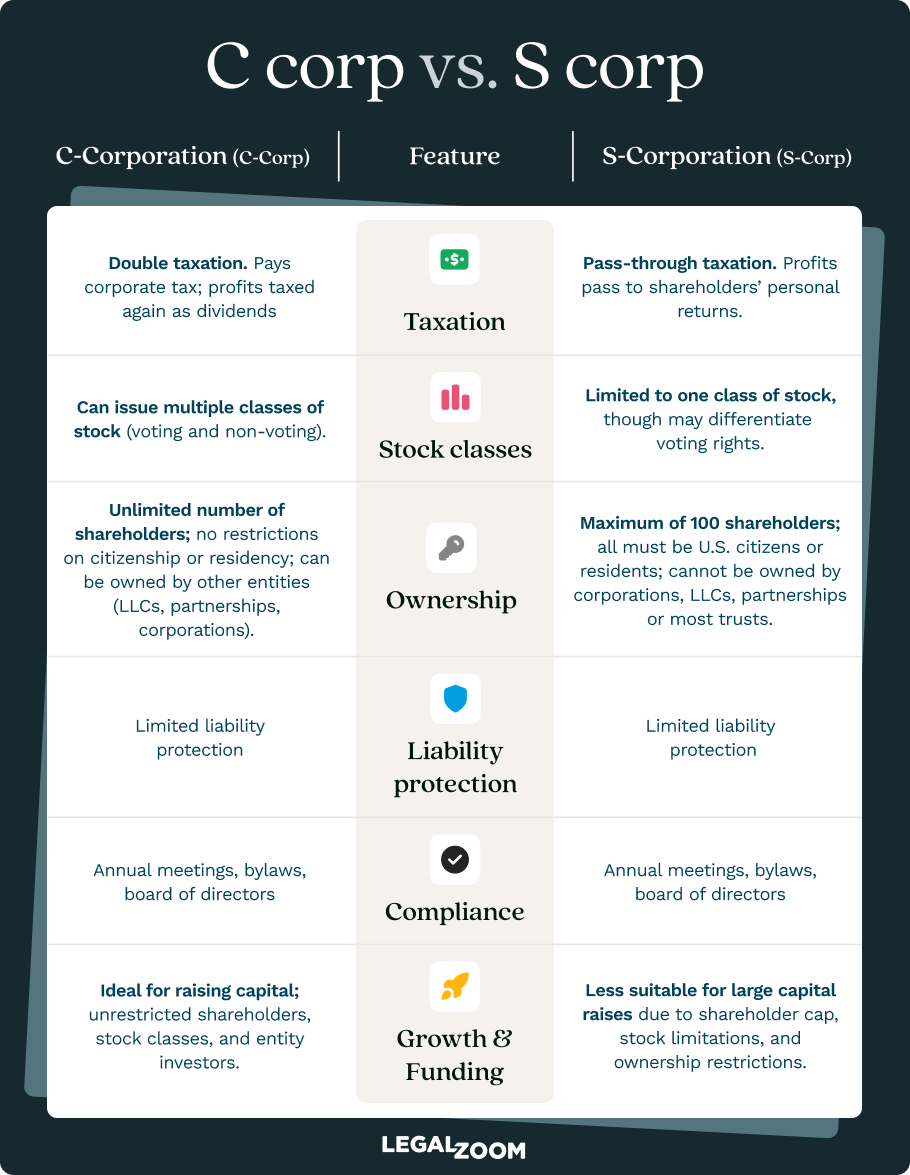

An S corp is a tax designation that allows business profits to pass directly to owners' personal tax returns, avoiding corporate-level taxation. Unlike C corporations, which pay corporate income tax before distributing profits to shareholders, S corps avoid this double taxation. Both corporations and LLCs can elect S corp status by filing Form 2553 with the IRS.

To be an S corp, your business must:

- Have no more than 100 shareholders

- Not have non-resident alien shareholders

- Not have owners that are corporations or partnerships

- Have only one class of stock

Electing S corp taxation involves filing Form 2553 with the Internal Revenue Service (IRS), though you’ll want to be mindful of the deadlines (more on this later).

Advantages of an S corp for LLC owners

When an LLC is taxed as a sole proprietorship or partnership, the owners are considered self-employed. Owners will pay Social Security and Medicare taxes (known as self-employment taxes) on their full share of the company's profits.

If your business earns significant profits, you may save on self-employment taxes by choosing S corp taxation instead.

S corp owners who work in the business can be company employees, and they must pay themselves a reasonable salary for the work they do. Like all employees, they'll pay Social Security and Medicare taxes on that salary, but additional company profits won't be subject to these taxes.

Owner-employees can also participate in company benefit programs, including 401K and profit-sharing plans. However, some employee benefits like medical and life insurance can be taxable if an employee owns more than two percent of the company.

There are a few main disadvantages for LLC electing S corp status.

- Additional paperwork: You must elect S corp status with the IRS and run payroll with tax withholdings.

- IRS scrutiny: The IRS closely monitors whether owner-employees pay themselves a fair and reasonable salary.

- Cost vs. benefit: For small businesses with few profits, these added burdens can outweigh the tax savings.

How salary and distributions affect self-employment tax

When your LLC operates under default tax treatment (as a sole proprietorship or partnership), you pay a 15.3% self-employment tax on your entire profit. With S corp taxation, the tax treatment splits into two categories:

- You must pay yourself a reasonable salary for the work you perform, which is subject to payroll taxes (the equivalent of self-employment tax, but processed through formal payroll).

- Any remaining profit can be distributed to you as an owner distribution. These distributions are not subject to the 15.3% self-employment tax—they're only subject to ordinary income tax.

Here's an example: If your LLC generates $120,000 in net profit and you elect S corp status, you might pay yourself a $70,000 salary (subject to payroll taxes) and take the remaining $50,000 as distributions. You'd save approximately $7,650 in self-employment tax on that $50,000 distribution (15.3% × $50,000), minus the additional costs of running payroll and maintaining S corp compliance.

However, you can't simply label most of your income a "distribution" and call it a day. Because the IRS expects owner-employees to be paid fairly for their work, understanding what counts as reasonable compensation is key to keeping the tax benefits.

Determining reasonable compensation and what the IRS looks for

The IRS requires that S corp shareholder-employees receive reasonable compensation for the services they provide to the business, but there's no fixed formula or safe-harbor percentage.

Instead, the IRS evaluates reasonable compensation using several criteria, such as:

- Training and experience. Your educational background, professional credentials, and years of experience in your field all influence what you should be paid. For instance, a seasoned consultant with 20 years of expertise would reasonably command a higher salary than someone just starting out.

- Duties and responsibilities. If you're the primary revenue generator, handle all client relationships, and manage operations, your salary should reflect that comprehensive responsibility.

- Time and effort devoted. How many hours do you work? Are you full-time or part-time? The time commitment directly impacts reasonable compensation expectations.

- Comparable salaries. What would you pay an unrelated third party to perform the same duties? Industry salary data, geographic location, and company size all factor into this comparison.

- Company profitability and financial condition. While a struggling business might justify lower compensation, a highly profitable S corp paying its owner-employee minimum wage while distributing hundreds of thousands in profits would likely raise red flags.

In practice, many tax professionals recommend that shareholder-employee salaries fall somewhere between 35%–50% of total business income, though this is a general guideline rather than a requirement. The key is documentation: maintain records showing how you determined your salary, including any salary surveys, industry comparisons, or professional advice you relied upon.

If the IRS determines your salary is unreasonably low, they might reclassify distributions as wages, assess back payroll taxes, and impose penalties and interest. The risk isn't theoretical—the IRS has won numerous cases where S corp owners paid themselves minimal salaries while taking substantial distributions.

C corp vs. S corp tax advantages

While large companies are typically C corporations, small business owners often prefer S corp taxation, because their profits aren't taxed at both the corporate and shareholder levels. However, S corp taxation isn't ideal for every business.

A company might benefit from C corp taxation if:

- It's a startup hoping to attract outside investment. Institutional investors usually prefer C corporations.

- It plans to keep money in the business to fund future growth. C corp shareholders only pay tax on money distributed to them, whereas S corp owners pay tax on all company profits.

- It doesn't meet the requirements for S corp taxation.

The tax advantages of an S corp depend on several factors, including your business' size, profitability, and structure. It's best to review your options with a tax professional who can help you make the right choice for your situation.

Is an S corp right for me?

Before you elect S corp status, it helps to run a quick break-even check to see when the savings typically outweigh payroll, tax prep, and compliance expenses. First, calculate the difference between paying 15.3% self-employment tax on all profit versus paying payroll taxes only on your reasonable salary. This gives you your gross annual savings.

Next, tally the incremental costs of S corp operation.

- Payroll processing: Running formal payroll (even for yourself) typically costs $500–$2,000 or more annually, depending on whether you use a payroll service or handle it yourself with software

- Additional tax preparation: S corp tax returns (Form 1120-S) are more complex than Schedule C filings, often adding more costs to your annual accounting fees

- State-level fees: Some states impose franchise taxes, annual report fees, or additional filing requirements on S corps

- Compliance risk: The cost of maintaining proper documentation, ensuring reasonable compensation, and staying current with payroll tax deposits

Beyond the numbers, your business must generate consistent, predictable profit. If your income fluctuates dramatically or you're just reaching profitability, the fixed costs of S corp compliance become harder to justify.

Moreover, the additional administrative burden—even if you outsource most of it—requires oversight and attention. If you're a solopreneur already stretched thin, the complexity may not be worth the savings.

When to file Form 2553 for new and existing entities

If you decide to move forward, you’ll want to time your S corp election correctly—missing the deadline can delay your intended tax treatment by a year and leave you on the hook for unnecessary taxes. The Form 2553 filing window depends on whether you're electing S corp status for a new entity or converting an existing business.

For newly formed LLCs or corporations:

- You must file Form 2553 within two months and 15 days after the beginning of the tax year in which you want the election to take effect. For most calendar-year businesses, this means filing by March 15 if you want S corp treatment for the current year.

- If you form your business mid-year, the clock starts from the beginning of its first tax year (generally when it first has shareholders, acquires assets, or begins business), and you have two months and 15 days from that date to file.

For existing LLCs or corporations:

- To elect S corp status for the upcoming tax year, you must file Form 2553 by March 15 of that year (for calendar-year taxpayers).

- If you miss this deadline, your election typically won't take effect until the following tax year unless you qualify for late S election relief.

There's an important exception: if you file Form 2553 at any time during the tax year before the year you want the election to take effect, the IRS will typically accept it (assuming you meet all other eligibility requirements).

Critical timing considerations:

- All shareholders must consent to the election by signing Form 2553 or a separate consent statement

- If you have a fiscal year rather than a calendar year, adjust the deadlines accordingly

- State-level S corp recognition may require separate filings and have different deadlines

- The election is effective for the entire tax year—you can't elect S corp status for just part of a year

Many business owners choose to file early in the fourth quarter of the preceding year. This approach eliminates deadline pressure, allows time to set up payroll systems, and ensures you're ready to operate as an S corp as soon as the new tax year begins.

If you're forming a new LLC specifically to operate as an S corp, you might consider filing Form 2553 simultaneously with your initial formation paperwork, which can prevent any gap in your intended tax treatment.

S corporation FAQs

What exactly is an S corp, and how is it different from a regular business?

An S corp is a tax designation where business profits "pass through" directly to shareholders' personal tax returns, avoiding the double taxation of C corps where both the business and owners pay taxes on the same income.

Who can choose S corp tax status, and what are the rules?

Your business can choose S corp taxation if it meets IRS requirements: no more than 100 shareholders, all of whom must be U.S. citizens or permanent residents, one class of stock, and no corporate or partnership owners.

How much money can I save on taxes with S corp status?

The biggest tax savings come from reducing self-employment taxes. Normally, business owners pay 15.3% in self-employment taxes on all their business profits for Social Security and Medicare. With S corp status, you only pay these taxes on the salary you pay yourself as an employee. Any extra profits you take out as distributions don't get hit with self-employment taxes.

What extra work and costs come with choosing S corp taxation?

Choosing S corp status creates significantly more paperwork and ongoing costs for your business. You'll need to set up payroll to pay yourself a regular salary, which means withholding taxes, filing quarterly reports, and potentially hiring a payroll service. You'll also need to follow corporate formalities like holding annual meetings, keeping detailed records, and filing additional tax forms. The IRS watches S corps closely to make sure salaries are reasonable, so you might face audits.

Should I choose S corp status for my LLC?

S corp taxation can be a smart choice for profitable LLCs, but it depends on how much money your business makes. However, choosing S corp taxation means giving up some of the flexibility that makes LLCs attractive. You'll also have to follow stricter rules about how you pay yourself and run your business.

How do I decide if S corp taxation is right for my business?

Start by looking at three key factors, including your annual profit, growth plans, and ability to handle extra paperwork. Consider your future plans—if you want to bring in investors, expand overseas, or have complex ownership arrangements. Finally, honestly assess whether you can handle running payroll, maintaining corporate records, and dealing with IRS scrutiny.

Even better, you can connect with a business attorney through LegalZoom’s network to get advice for your situation.

Edward A. Haman, Esq. contributed to this article.

'%20/%3e%3c/svg%3e)

'%3e%3cpath%20fill-rule='evenodd'%20clip-rule='evenodd'%20d='M9.31239%2025.5316H13.0679V14.1032H9.31239V25.5316ZM11.1913%208.46875C9.93945%208.46875%209%209.25086%209%2010.505C9%2011.5995%209.78211%2012.5389%2011.1913%2012.5389C12.6005%2012.5389%2013.3826%2011.5995%2013.3826%2010.505C13.3826%209.4082%2012.6005%208.46875%2011.1913%208.46875ZM27%2018.9577V25.5316H23.2445V19.4275C23.2445%2017.8609%2022.6174%2016.7664%2021.3679%2016.7664C20.2711%2016.7664%2019.644%2017.5463%2019.3316%2018.1756C19.1743%2018.488%2019.1743%2018.8004%2019.1743%2019.1128V25.5316H15.4165V13.9458H19.1743V15.5123C19.644%2014.7302%2020.5835%2013.6357%2022.6174%2013.6357C25.1234%2013.7908%2027%2015.3573%2027%2018.9577Z'%20fill='white'/%3e%3c/g%3e%3cdefs%3e%3cclipPath%20id='clip0_952_9489'%3e%3crect%20width='18'%20height='18'%20fill='white'%20transform='translate(9%208)'/%3e%3c/clipPath%3e%3c/defs%3e%3c/svg%3e)