Limited liability companies (LLCs) and S corporations are two types of business structure, but they work very differently: An LLC is a business entity while an S corp is a tax classification available to some businesses. If you’re considering starting a business, you’ll want to sort out the differences between these two so you can make the best financial decision for your situation.

This guide provides a thorough comparison of LLC vs. S corp status, plus tips for choosing your business structure.

Key takeaways

- Limited liability companies and S corporations offer different taxation benefits and management structures.

- Both LLCs and S corporations offer liability protection that safeguards owners’ personal assets from business debts and legal issues.

- LLCs have more management flexibility than S corporations and fewer compliance requirements.

- Consider your business needs, assess your financial situation, and consult with legal or tax professionals when deciding which legal entity/tax classification best suits your business's risk level, asset protection, and management needs.

What is an LLC?

A limited liability company (LLC) is a legal business structure that can protect small business owners from personal liability in business obligations. This is a key feature of LLCs and sets them apart from sole proprietorships and partnerships, which don’t have limited liability protection. Owners of LLCs are known as members. Limited liability companies can have one owner (single-member LLC) or more than one owner (multiple-member LLC).

Here are the main elements of an LLC:

- A formal business structure that must register with the state

- Generally good protection from personal liability for business debts

- Flexible ownership and few formal requirements

- Default pass-through tax classification

LLC taxation

By default, LLCs are taxed as pass-through entities, where profits and losses pass through to the owners’ personal tax returns. Standard taxation for LLCs mirrors sole proprietorships (for single-member LLCs) and partnerships (for multiple-member LLCs). The benefit of pass-through taxation is that it avoids the double taxation experienced by C corporations, wherein both the corporation and its shareholders are taxed). However, owners of pass-through entities must pay a 15.3% self-employment tax on all net profits.

Single- and multiple-member LLCs can also elect to be taxed as C corporations or S corporations if they meet eligibility requirements.

LLC flexibility and formalities

Overall, an LLC is more flexible than a corporation in organization, leadership decisions, and profit distribution, all of which are typically laid out in an operating agreement. An operating agreement is an internal document used to clearly lay out the rules for how your company will be run. It’s not required by state law but is helpful for preventing disputes.

LLCs also have fewer compliance requirements than corporations. For instance, LLCs do not have to write bylaws or adhere to other corporate management requirements. They aren’t required to have mandatory annual meetings or take meeting minutes, plus, there are fewer requirements for recordkeeping. However, most LLCs must submit annual reports to the state agency that oversees business formation and pay a franchise tax in some states.

LLC ownership and management

LLCs can choose from two management models:

- Member-managed: LLC members (owners) manage the various aspects of the business

- Manager-managed: LLC members hire one or more managers to manage the business

For LLC members that want to play an active role, member-managed is the best choice. But if the members lack management expertise or are predominantly serving as investors, it may be beneficial to opt for a manager-managed LLC structure.

LLC ownership is also flexible. An LLC can have unlimited members worldwide, and these owners can also be another corporate entity. There are no restrictions on classification or nationality.

LLC benefits: The bottom line

An LLC protects owners’ personal assets while keeping operations simple. Here is an overview of the main benefits of an LLC:

- Limited liability protection for members. This means that if the business owes money to a creditor, the owner's personal assets will not be used to pay off that debt.

- Flexible ownership and management. There are no limits on the number of LLC members, and they don’t have to be U.S. residents. LLCs can be member- or manager-managed.

- Simple setup and few compliance requirements. LLCs typically have less formation paperwork and fewer ongoing legal obligations compared to corporations.

- Flexible profit allocation. LLC can choose how profits are distributed to members. For example, profits can be allocated based on work contributions instead of by ownership percentage.

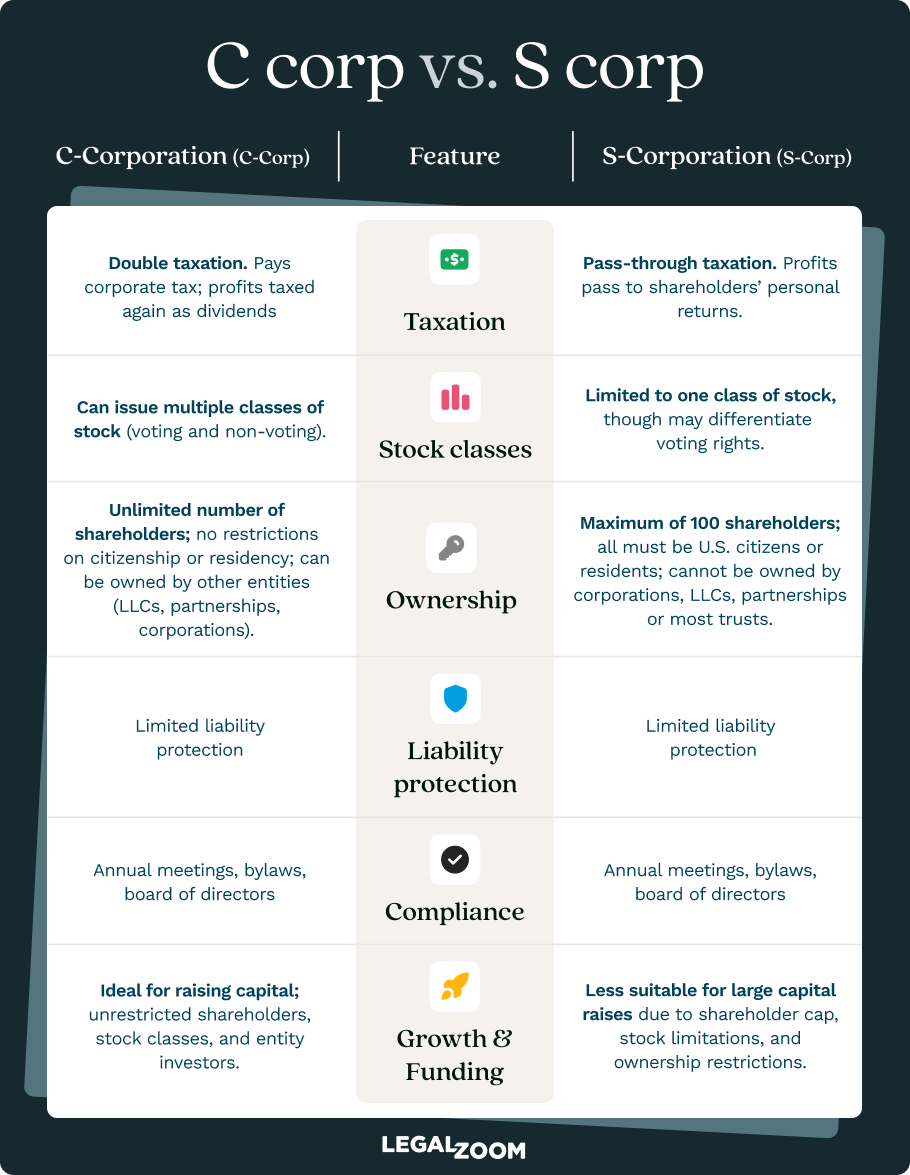

What is an S corporation?

An S corporation is a tax classification for a qualifying corporation or LLC that can protect small business owners' assets from double taxation. It gets its name from its definition in subchapter S of the Internal Revenue Code. An S corp utilizes pass-through taxation, meaning an owner claims a share of company profits on their return when they file taxes. This tax classification also helps shareholders avoid double taxation at the federal level by passing income directly to their personal income tax returns.

According to the Internal Revenue Service, you must meet the following requirements to elect S corp status:

- Gain consent from LLC members to convert to S corp election

- Be a U.S. business

- Have no more than 100 shareholders (who are not corporations, partnerships, or non-resident aliens)

- Have only one class of stock

- Can not be a financial institution, insurance company, or other ineligible corporation

S corp taxation

Business owners that elect S corp taxation are essentially treated as company employees, meaning that they must pay themselves a reasonable salary for their work.

“When determining what a reasonable salary looks like, you have to look at the practical reality of the business. If the numbers don't reflect a livable wage for the work being done, it likely won't be viewed as reasonable. ”

Business Attorney

Under S corp taxation, business owners pay federal income taxes and state income taxes, Medicare, and Social Security tax on that salary. Owners receive additional profits as distributions, which aren't subject to Medicare and personal income tax or Social Security taxes.

The major advantage of an S corporation is avoiding having to pay self-employment taxes on a portion of the owner's income. In an S corp, only owner-employee salaries are subject to taxes for Social Security and Medicare. Any additional profits distributed to shareholders are not subject to these taxes, which can result in significant tax savings. This contrasts with an LLC, where owners may be subject to self-employment tax on all net earnings from the business.

S corp formalities and structure

The management for an S corp is a bit more complex than for an LLC. It requires a formal structure that includes a board of directors and corporate officers. The number of directors on the board varies according to state law, but most states require at least one director. Officers are appointed by the S corp owner to manage different aspects of the business. However, it’s just fine for one person to hold owner, director, and officer roles, in the case of one entrepreneur who elected S corp taxation.

Most states mandate that corporations, including S corporations, conduct annual shareholder and board meetings and document the information through meeting minutes, which act as legal proof of any formal changes to the business and that you’re serving in the best interest of the shareholders. This requires more recordkeeping than an LLC.

Additionally, every S corp must create corporate bylaws that essentially dictate business operations and procedures.

S corp ownership restrictions

An S corp must be a U.S. business owned by U.S. citizens or residents and cannot have more than 100 shareholders. Beyond individuals, trusts and estates can also be owners of S corporations.

Like a C corporation, an S corp can issue stock. They can only issue common stock with shareholder voting rights.

S corp benefits: The bottom line

There are several advantages of choosing an S corp election:

- Pass-through taxation. S corporations are not subject to corporate income tax, meaning that they're not double taxed.

- Potential to reduce tax burden. S corp owners can split their compensation into salary + distributions, helping to reduce taxable income.

- Credibility and investor attraction. A formal corporation status and ability to issue stock can appeal to banks and investors.

- Personal liability protection. S corp owners’ and shareholders’ personal assets, such as their personal bank accounts or their home, cannot be taken in the case of debts or litigation.

LLC vs. S corp: How are they similar?

LLCs and S corporations share some similarities in both features and legal requirements:

- Limited liability. Both limited liability companies and S corporations provide limited liability protection, ensuring owners and shareholders are not personally responsible for the business's debts and liabilities. The extent of liability coverage may be stronger with a corporation due to the stricter compliance requirements. But ultimately, both LLCs and S corporations provide substantial liability protection.

- Pass-through tax advantages. Both LLCs and S corporations enjoy pass-through taxation, where profits and losses are passed through to personal tax returns.

S corp vs. LLC: Key differences

The main difference between an LLC and S corp is that an LLC is a business structure, whereas an S corp is a tax status. So, business owners cannot form an S corp with their state; instead, they form an LLC or a C corporation, then they can elect to be taxed as an S corporation.

Beyond this key distinction, there are also other differences between an LLC and an S corp.

- Taxation: S corporations can provide a tax benefit by allowing owners to pay themselves a salary, while LLC owners are subject to self-employment taxes on their entire income. However, any S corp employees earning a salary must pay payroll taxes.

- Ownership: LLCs can have an unlimited number of members, who can be nonresidents. An S corp can only have up to 100 owners/shareholders, who must be U.S. citizens or residents, or U.S.-based trusts.

- Profit allocation: LLCs can distribute profits as members see fit, while S corp distributions must be based on shareholders’ ownership percentages.

- Management: S corporations have a more rigid structure than LLCs, requiring a board of directors and corporate officers to manage the company. LLCs don’t have this requirement.

- Investor appeal: Business entities that have S corporation status are more appealing to investors than LLCs because of the formalities, structure, and ability to issue stock.

- Transferability of ownership interests: Transferring ownership is typically more straightforward with an S corp because of stocks and clear processes set in the company bylaws. This may be more difficult with an LLC if clear ownership percentages aren’t used or the operating agreement doesn’t detail the process.

How to choose: LLC or S corp?

When deciding whether to elect S corp status or keep your current LLC structure, it can be helpful to first ask yourself the following questions to understand which is right for you:

- How many owners have a stake in your business?

- Are all of your business partners U.S. citizens or residents?

- Does a partnership or corporation have a stake in your business?

- How would a self-employment tax affect your net profit?

When to choose an LLC

You may want to establish an LLC if you're concerned about personal liability, your profits are relatively low, and you want a simple business structure with fewer compliance requirements.

Remember that this type of business structure offers more flexibility in management and profit allocation, allowing owners to manage the business as they see fit. Furthermore, paperwork and reporting requirements are generally simpler for an LLC than for an S corp, which has stricter compliance regulations. LLCs are also a good option for individuals who want to start or invest in a company in the United States but who aren’t U.S. citizens or residents.

“If your profession doesn’t restrict you from being an LLC and you’re not trying to bring on investors, a lot of the time an LLC makes more sense. It still provides you liability protection, but it’s not as cumbersome as a corporation.”

Business Attorney

When to choose an S corporation

S corp tax classification might be best for your business if you have plans to scale. LLCs may face limitations in raising capital due to their inability to issue stock. Because an S corp can issue stock, it’s easier to attract investors and secure funding for expansion.

It’s also important to consider how much your business earns, as a 15.3% self-employment tax levied on an LLC's profits can become steep when revenues begin to tick upward. S corp status may be beneficial if your business earns enough to benefit from splitting salary and dividends for tax savings.

Companies with an annual profit of $80,000 or greater may find that electing S corp status can result in tax savings. By converting to an S corp, owners can potentially reduce the business income subject to self-employment tax, thereby decreasing their total tax payments. This could greatly benefit businesses generating substantial profits, as tax savings can be reinvested or distributed to S corporation shareholders. Nonetheless, it's crucial to balance these potential tax savings against the added complexity and compliance requirements to take advantage of S corp status before deciding.

While financial professionals usually agree that lower profits means fewer tax savings with an S corp, there’s no magic number. It’s best to consult a financial advisor or tax professional to determine what’s best for your situation.

Costs and administrative burden

There are major differences in administration and management when electing S corp versus LLC standard tax status. Below are some differences to consider.

Formation costs and paperwork

For an S corp, you'll first form a C corp or LLC that must meet S corp classification requirements. Formation involves filing your articles of incorporation with the Secretary of State or relevant state agency. This document includes necessary information about the business. Filing fees vary by state and range from $45 to $315.

Once you receive a certificate of formation, you must elect S corp status by filing Internal Revenue Service (IRS) Form 2553 within 2 months and 15 days after officially organizing your business in order for the status to affect the current tax year. You must also cap ownership at 100 individuals (not entities or partnerships) and limit those owner shares to U.S. citizens or residents only. All shareholders must consent to the subchapter S election.

To form an LLC, you’ll need to submit articles of organization to the state (typically the Secretary of State’s office) and pay the filing fee. Formation fees range from $45 to $500, and processing times can take anywhere from a couple of minutes to a few weeks, depending on the agency and whether filing is done online or by mail.

If you do business in other states as an LLC, you'll need to register to conduct business in each additional state and pay their foreign business registration fee.

Annual costs and reporting

States have different annual costs and reporting requirements. For instance, some states institute a franchise tax on all business entities and tax classifications, while others don’t have franchise taxes or limit them to only certain designations. Most states require filing annual reports, but details, information, and deadlines vary.

Check with your state to determine what obligations your business has.

Bookkeeping requirements

S corporations have stricter ongoing bookkeeping requirements than LLCs. While the IRS shares general tips for what all small business owners should keep track of (like income and business expenses), S corporations must also keep track of “reasonable salary” for shareholders considered employees, payroll records, distribution records, and shareholder meeting minutes.

Registered agent services

Both LLCs and S corporations must designate a registered agent (sometimes called a resident agent), who serves as the business’s point of contact for legal and government correspondence. Business owners can designate themselves as a registered agent, another individual, or a company. LegalZoom’s registered agent services align with state requirements and help to ensure that you get important paperwork and notices in a timely manner.

S corp vs. LLC FAQs

Can an LLC elect S corp taxation?

Yes, it is possible to convert an existing LLC to an S corp, given that the LLC meets the IRS requirements to elect S corp status. This process first requires filing articles of incorporation conversion paperwork with your state, then electing S corp status by filing Form 2553 by March 15.

Can an S corp own an LLC?

Yes, an S corp can own an LLC. This is possible because LLCs enjoy flexible ownership.

Who can be an S corp shareholder?

An S corp shareholder must be a U.S. citizen or resident, or eligible trust or estate.

Does my state recognize S corp status?

S corporation tax status is a federal election, not a state election. Therefore, all states allow S corp designations. However, differences may lie in the conversion process.

Are S corp distributions subject to payroll tax?

S corp distributions are not subject to payroll taxes—only the salary is subject to payroll tax.

How do profit allocations work?

LLCs can allocate profits as they fit, whether that’s by amount of work or past performance. S corporations, on the other hand, must distribute profits based on ownership percentage.

Halona Black contributed to this article.

'%20/%3e%3c/svg%3e)

'%3e%3cpath%20fill-rule='evenodd'%20clip-rule='evenodd'%20d='M9.31239%2025.5316H13.0679V14.1032H9.31239V25.5316ZM11.1913%208.46875C9.93945%208.46875%209%209.25086%209%2010.505C9%2011.5995%209.78211%2012.5389%2011.1913%2012.5389C12.6005%2012.5389%2013.3826%2011.5995%2013.3826%2010.505C13.3826%209.4082%2012.6005%208.46875%2011.1913%208.46875ZM27%2018.9577V25.5316H23.2445V19.4275C23.2445%2017.8609%2022.6174%2016.7664%2021.3679%2016.7664C20.2711%2016.7664%2019.644%2017.5463%2019.3316%2018.1756C19.1743%2018.488%2019.1743%2018.8004%2019.1743%2019.1128V25.5316H15.4165V13.9458H19.1743V15.5123C19.644%2014.7302%2020.5835%2013.6357%2022.6174%2013.6357C25.1234%2013.7908%2027%2015.3573%2027%2018.9577Z'%20fill='white'/%3e%3c/g%3e%3cdefs%3e%3cclipPath%20id='clip0_952_9489'%3e%3crect%20width='18'%20height='18'%20fill='white'%20transform='translate(9%208)'/%3e%3c/clipPath%3e%3c/defs%3e%3c/svg%3e)