A living trust, also known as a revocable trust, is an important tool for estate planning. When you create a living trust, you, as the trust's grantor, place your assets into the trust, but you retain the full benefit of those assets during your lifetime. Upon your death, these assets are then transferred to the trust's beneficiaries.

Unlike in a fixed or irrevocable trust, the grantor in a living trust retains the right to change the terms of the trust, such as by designating new beneficiaries. A grantor can make such changes at any time.

What is the difference between a primary beneficiary and a contingent beneficiary?

A primary beneficiary receives trust assets first, while a contingent beneficiary receives them only if the primary beneficiary is unable or unwilling to accept them. A living trust can be either a single-grantor trust or a joint living trust. When setting up your trust, it's important to know the difference between the two, because it can affect who ultimately gets the trust's assets.

A primary beneficiary is any person or entity designated by the trust to receive its assets. In general, being a primary beneficiary means you receive distributions from the trust during the trust's existence. However, if it is a discretionary trust, the individual who both legally owns and manages the trust, known as the trustee, decides when and to which beneficiaries distributions are made.

Unlike a primary beneficiary, a contingent beneficiary is a person or entity who becomes entitled to receive trust assets only if the primary beneficiary is unable or chooses not to do so. For example, if the primary beneficiary dies or can't be found, the contingent beneficiary becomes entitled to distributions from the trust.

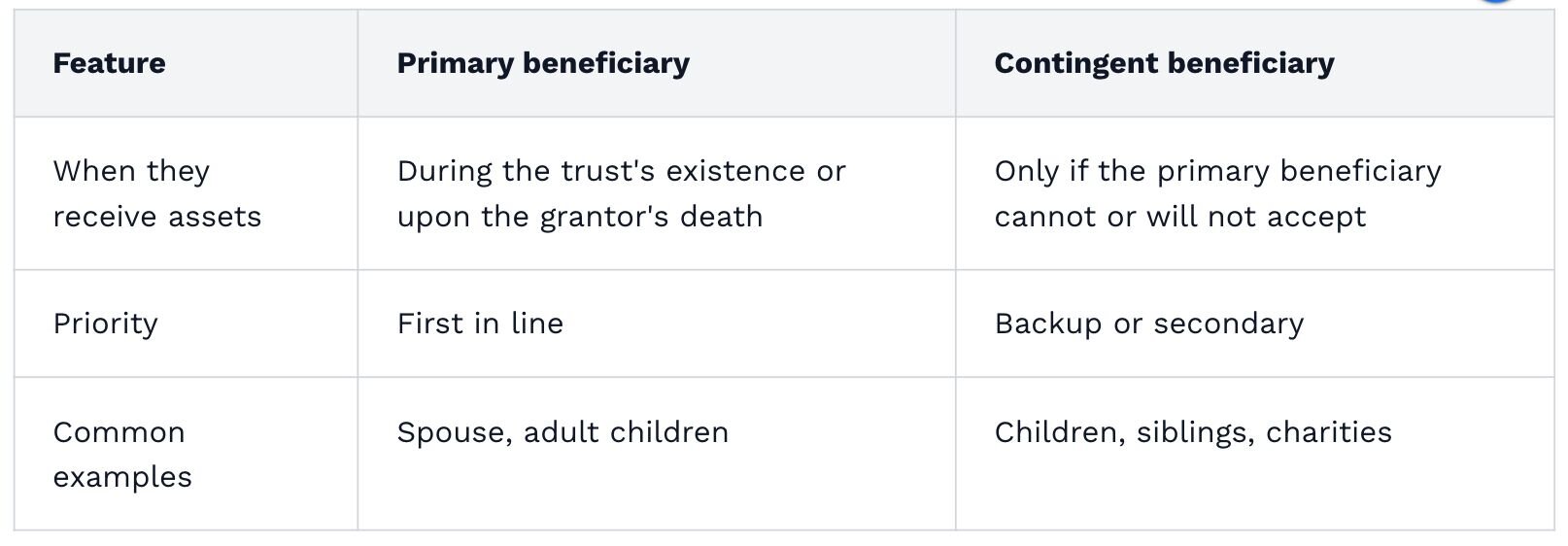

| Feature | Primary Beneficiary | Contingent Beneficiary |

|---|---|---|

| When they receive assets | During the trust's existence or upon the grantor's death | Only if the primary beneficiary cannot or will not accept |

| Priority | First in line | Backup or secondary |

| Common examples | Spouse, adult children | Children, siblings, charities |

How to allocate percentages among beneficiaries

When you have multiple primary or contingent beneficiaries, you'll need to specify what percentage of assets each person or entity receives. For example, you might designate your spouse as the sole primary beneficiary at 100%, then name your three children as contingent beneficiaries at 33.3% each. Alternatively, you could split primary beneficiary status between your spouse (60%) and a sibling (40%).

Your percentages must total exactly 100% within each beneficiary tier to avoid confusion or legal disputes. If one beneficiary in a percentage split predeceases you, what happens to their share depends on how you've structured your trust. You can specify that the deceased beneficiary's share passes equally to the remaining beneficiaries in that tier, or that it moves down to the contingent beneficiary level.

Review and update your percentage allocations after major life events such as births, deaths, marriages, or divorces. A percentage split that made sense when you had two children may need to be adjusted after a third child is born.

Can a trust be a contingent beneficiary?

Yes, a trust can serve as a contingent beneficiary for your living trust, life insurance policies, or retirement accounts. This strategy is particularly useful when you want to maintain control over how and when assets are distributed rather than passing them directly to individuals.

Naming a trust as a contingent beneficiary offers several advantages. If your contingent beneficiaries include minors, the trust can hold and manage assets until they reach an age you specify, such as 25 or 30, rather than distributing everything when they turn 18. A trust can also provide creditor protection for beneficiaries and ensure that assets stay within your family line if a beneficiary divorces.

This approach works well in specific scenarios: when your primary beneficiary is elderly and your ultimate intended recipients are minors, when you have a beneficiary with special needs who might lose government benefits from a direct inheritance, or when you want to protect a beneficiary who struggles with financial management. The trust document can include detailed instructions about distributions, giving you peace of mind that your wishes will be carried out.

All beneficiaries are subject to the same tax implications when receiving income from a trust. When a beneficiary receives a trust distribution, they must pay taxes on that income. The amount of tax depends on their personal tax rate.

What is a contingent beneficiary in life insurance?

Designating beneficiaries for your life insurance is an important part of the estate planning process. While most people remember to designate a primary beneficiary, it's also important to choose contingent beneficiaries.

If your primary beneficiary dies before you do and you haven't designated a contingent beneficiary, the proceeds will be paid into your estate. This creates problems.

- Probate delays: Insurance proceeds are subject to probate, which can take months or years.

- Additional costs: Probate fees and court costs reduce the amount your loved ones ultimately receive, with trust administration costing 60–80% less than probate.

What happens if you don't name a contingent beneficiary

The consequences of not naming a contingent beneficiary extend beyond life insurance to your living trust as well. If your primary beneficiary cannot inherit and no contingent beneficiary exists, your trust assets may be distributed according to the trust's residuary clause, if one exists, or pass through probate and be distributed under your state's intestacy laws.

Probate typically takes 6 to 18 months, though contested cases take two to three times longer. During this time, your family may not have access to the funds they need. The costs are substantial too: probate fees, attorney costs, and court expenses often total 2% to 7% of the estate's value. For a $500,000 estate, that could mean $10,000 to $35,000 in fees that would otherwise go to your loved ones.

Without a contingent beneficiary, you also lose privacy. Probate is a public process, meaning anyone can access information about your assets and who inherited them. Perhaps most importantly, you lose control over who receives your assets. State intestacy laws follow a rigid formula that may not reflect your wishes—a distant relative you've never met could inherit while a close friend or stepchild you wanted to provide for receives nothing.

Can minors be contingent beneficiaries?

Children are often designated as contingent beneficiaries under a living trust. In such cases, the trust pays distributions, usually in the form of income, to the primary beneficiary, often the surviving spouse, and the children are entitled to any remainder of the trust upon that primary beneficiary's death.

Sometimes, family trusts are structured so that children who are contingent beneficiaries become primary beneficiaries upon reaching the age of majority.

Appointing a guardian for minor beneficiaries

In all cases where a minor child is a beneficiary of a trust, you should also appoint a legal guardian to manage whatever proceeds or assets the child receives until they are of legal age. It is a critical step.

Do you need a contingent beneficiary?

While not legally required, contingent beneficiaries are strongly recommended for virtually every living trust. The effort required is minimal, typically just adding a few lines to your trust document, while the protection it provides is substantial.

Contingent beneficiaries are especially critical in certain situations.

- Your primary beneficiary is elderly or in poor health: The likelihood that they may predecease you or be unable to inherit increases.

- Your primary beneficiary works in a high-risk occupation: First responders, military personnel, or those in dangerous professions face elevated mortality risks.

- You have significant assets: The larger your estate, the more your loved ones stand to lose in probate fees and delays.

- Your primary beneficiary is also a minor: Children face unique legal complications that make backup planning essential.

- You're unmarried or have no children: Without obvious heirs, state intestacy laws may distribute your assets in unexpected ways.

Even if none of these situations apply to you, circumstances change. A healthy 45-year-old primary beneficiary today could face a serious illness in 10 years. By naming contingent beneficiaries now, you protect your estate plan against unpredictable events without constantly updating your documents.

Who should you name as a contingent beneficiary?

It’s important to give serious thought to who you’d want to receive your assets if your primary beneficiary couldn't. The most common choices follow a natural family hierarchy: When a spouse is the primary beneficiary, adult children typically serve as contingent beneficiaries. When children are young, siblings or parents often fill the contingent role.

Consider these factors when making your selection.

- Financial responsibility: Can the potential beneficiary manage a significant inheritance, or would they benefit from receiving assets through a trust?

- Age and life stage: Naming a beneficiary much older than you increases the chance they'll predecease you. Naming someone very young means assets may need to be managed on their behalf for years.

- Family dynamics: Consider whether your choice might create conflict among family members and whether that matters to you.

- Geographic location: If you own real property, a local beneficiary may be better positioned to manage or sell it.

You can name multiple contingent beneficiaries and specify how assets should be divided among them. Consider using a "per stirpes" designation, which means if one of your contingent beneficiaries dies before you, their share passes to their children rather than being redistributed among the surviving contingent beneficiaries. This approach keeps assets flowing down family lines as many grantors intend.

Charitable organizations also make excellent contingent beneficiaries, particularly if your primary and other contingent beneficiaries are all similar in age to you. Naming a charity ensures your assets go to a meaningful cause rather than through probate if the unexpected happens.

FAQs on contingent beneficiaries in a living trust

What rights does a contingent beneficiary have in a trust?

Contingent beneficiaries generally have limited rights compared to primary beneficiaries; they typically cannot request trust accountings unless the trust grants that right, though they can petition to remove a trustee for mismanagement. State laws vary, with some requiring trustees to provide accountings to contingent beneficiaries as well.

When setting up a living trust, it's always a good idea to designate one or more contingent beneficiaries. Doing so gives you peace of mind about what will happen to your assets after you die.

Belle Wong, J.D., contributed to this article.

'%20/%3e%3c/svg%3e)

'%3e%3cpath%20fill-rule='evenodd'%20clip-rule='evenodd'%20d='M9.31239%2025.5316H13.0679V14.1032H9.31239V25.5316ZM11.1913%208.46875C9.93945%208.46875%209%209.25086%209%2010.505C9%2011.5995%209.78211%2012.5389%2011.1913%2012.5389C12.6005%2012.5389%2013.3826%2011.5995%2013.3826%2010.505C13.3826%209.4082%2012.6005%208.46875%2011.1913%208.46875ZM27%2018.9577V25.5316H23.2445V19.4275C23.2445%2017.8609%2022.6174%2016.7664%2021.3679%2016.7664C20.2711%2016.7664%2019.644%2017.5463%2019.3316%2018.1756C19.1743%2018.488%2019.1743%2018.8004%2019.1743%2019.1128V25.5316H15.4165V13.9458H19.1743V15.5123C19.644%2014.7302%2020.5835%2013.6357%2022.6174%2013.6357C25.1234%2013.7908%2027%2015.3573%2027%2018.9577Z'%20fill='white'/%3e%3c/g%3e%3cdefs%3e%3cclipPath%20id='clip0_952_9489'%3e%3crect%20width='18'%20height='18'%20fill='white'%20transform='translate(9%208)'/%3e%3c/clipPath%3e%3c/defs%3e%3c/svg%3e)