Retirement is exciting, but it can also provoke feelings of worry and anxiety as you consider your financial stability and what that will look like down the road. Luckily, there are strategies you can take advantage of to calm your mind to live comfortably during those years.

Keep reading to learn about considerations that will help you determine if you're ready for retirement, as well as additional retirement tips and resources before you choose your retirement date.

How to figure out when you can retire

There are many ways to help you determine when you can retire. This includes figuring out several factors, such as:

- Your current financial status

- Social Security benefits

- Amount of debt

- Future expenses

- Inflation

- Current employment status

- Retirement account status

Read on to explore these considerations in more detail.

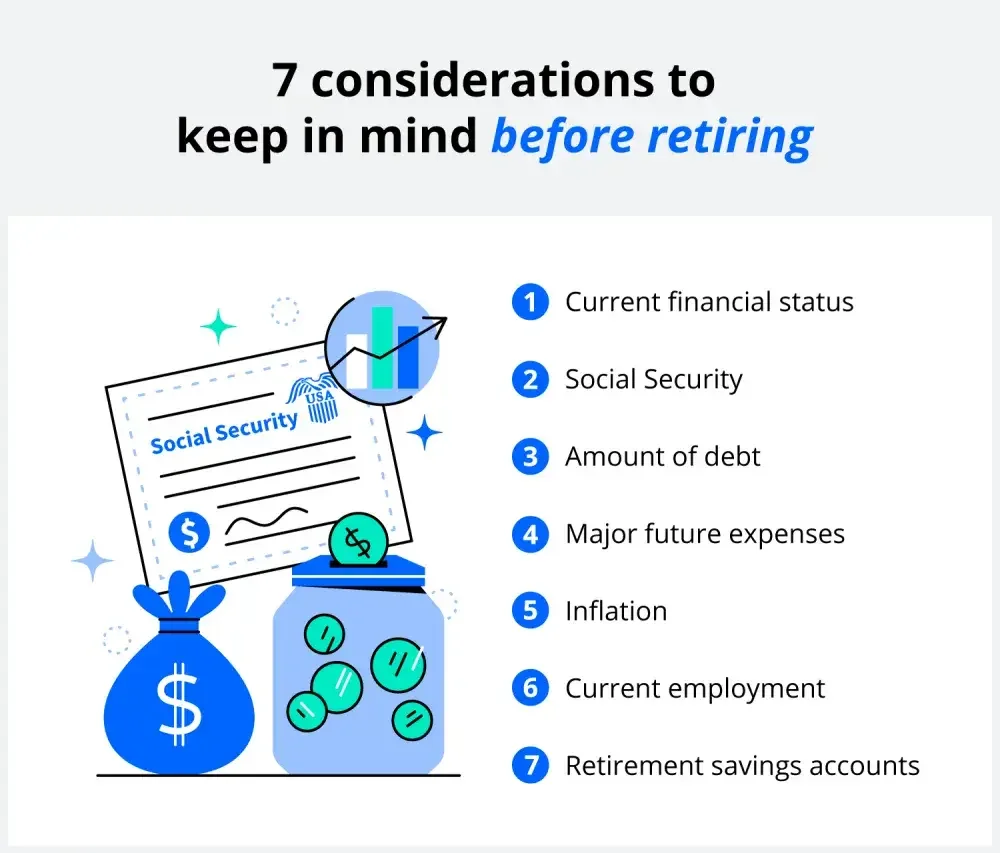

7 retirement considerations to keep in mind

The average age of retirement in the United States is 67. If you're approaching this age and wondering whether or not you are ready to retire, you're not alone. Here are seven considerations to keep in mind before retirement:

1. Current financial status

When you ask yourself, "Can I retire?" the first thing you'll need to consider is if you'll have enough savings and will be able to pay your bills. You will need to calculate how much you need in savings to retire and how much you need to save to stay financially stable during retirement.

How much do I need to retire?

There is no set amount of money that you need for retirement—it depends on different variables, such as:

- Current lifestyle

- The cost of living where you live

- Health needs

- Other obligations

As a general rule, many experts say that your monthly income while in retirement should be around 80% of the income of your last job, or somewhere around $1 million. This will vary based on your situation, however, and may require more or less depending on if you still need to pay off a mortgage or similar payment.

Calculate your finances

To calculate how much you need in savings, take your current household income and multiply that by 0.8. Then, divide your result by 12 to determine your monthly payment needs while in retirement. Next, you can adjust that number to be higher or lower based on what you want to do in retirement, whether traveling, taking on an expensive hobby, or simply saving more.

For example, if your household income is $80,000, you would multiply that by 0.8 to come up with $64,000. After dividing that by 12, the result would be $5,333.

2. Social Security

Social Security is a benefit included in American workers' retirement plans. This benefit aims to provide replacement income for qualified retirees and their families. By age 62, you can start receiving some Social Security benefits. Make sure to include this benefit when considering if you can retire and how much money you'll have going into it.

How much will I get from Social Security?

The amount you receive from Social Security depends on your lifetime earnings—a higher income will give you a larger benefit. As of April 2022, the average Social Security benefit is $1,538.14 monthly. The maximum amount you can get is $3,345 a month.

The amount is also determined by what age you claim these benefits. You can start receiving benefits at age 62, but if you sign up at file retirement age (FRA), which is 66 or older depending on your birth year, you can receive 100% of the benefit calculated from your earnings history.

3. Determine the amount of debt you have

Having to pay off debt while in retirement can shave off your hard-earned savings and can limit the amount of freedom you have.

If you have debts to pay off, you'll need to weigh the benefits and costs of saving for retirement vs. paying off debt. Fortunately, there are steps you can take to pay down debt before you retire. Some debts to prioritize taking care of before retirement include:

- Mortgage

- Student loans

- Car loans

- Credit card bills

If you cannot pay off all debt before retirement, don't stress. But make sure you're doing all you can to pay off your highest-cost debts and prioritize saving.

4. Major future expenses

Think if you have any major upcoming expenses that you may need to cover. This could include:

- A new car

- Down payment on a house

- College tuition and education

- Mortgage payoff

- Vacations

If you anticipate a large expense that will cause you to dip into your savings, consider holding off on retirement for a little bit longer, so you have some extra time to save. While doing so, keep in mind the expenses you'll have in retirement—this can help you determine how much you need to save for that large expense.

Unavoidable retirement expenses

These expenses are essential costs that you'll need to account for when considering retirement. These must-haves include:

- Housing costs

- Health care

- Groceries

- Utilities

- Transportation

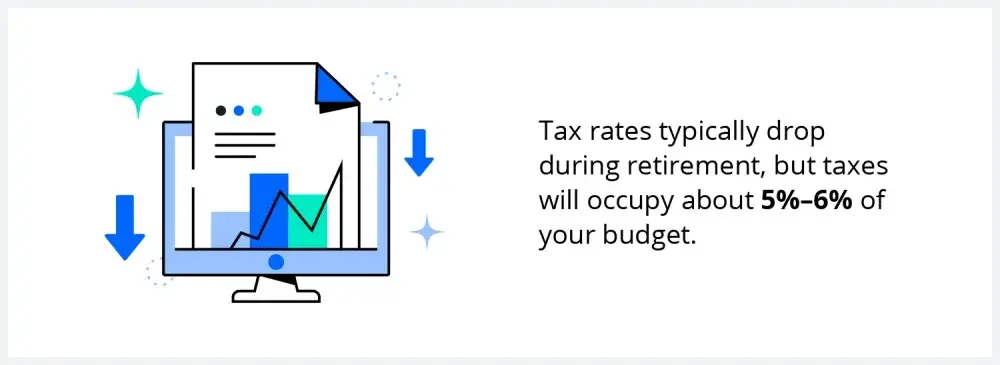

- Taxes

- Debt payments (if applicable)

- Other miscellaneous payments that are mandatory

Depending on the state, you may have to pay taxes for your Social Security benefits if you receive an income stream from another source.

What should my budget look like for nonessential expenses?

You should also consider a budget for the nonessential necessities, such as:

- Travel

- Entertainment

- Clothes

- Home services or housekeeping

- Dining out

- Home furnishings

If you're in a pinch, these should be the first expenses cut from your spending budget. But if you have extra wiggle room, you can boost your budget in these categories.

5. Inflation

Before retiring, consider current inflation and the possibility of inflation in the future. Inflation can affect your budget, so it's important to check in every few years to see if you're still on track when it comes to your savings. Your Social Security benefits provide a nice cushion for inflation, but it's still something to consider.

6. Retirement savings accounts

The best way to save for retirement is with retirement savings accounts. These accounts include:

- 401(k)

- Roth IRA

- Pensions

Be sure to consider these accounts when it comes to your total savings. At age 59 ½, you can start taking money out of your IRA or 401(k)—if you withdraw any sooner than that, you'll face hefty penalties and tax requirements, usually with a 10% penalty.

7. Current employment

Lastly, you should consider if it's worth leaving your current employer. Staying employed for longer can help you close the gap between what you have in savings and what you still need to retire.

A part-time job may help reduce how much money you need to take out of your savings.

Keeping a part-time job can also make it easier for you to transition into the full-time job market again in case of an emergency and you need extra money. You might also consider starting a business in retirement so you can control your hours. Here are some part-time job ideas for retirees—these are also great if you're unable or not ready to retire fully yet:

- Bookkeeper

- Dental hygienist

- Office manager

- Administrative assistant

- Secretary

- Registered nurse

- Paralegal

- Merchandise displayer

- Retail sales worker

- Sales associate

- Cashier

Common retirement calculations and formulas

There is no one-size-fits-all answer when it comes to whether or not you can retire, but there are some tips and tricks you can follow.

Formula to help calculate how much you need to retire

Many experts say that your monthly income while in retirement should be around 80% of the income from your last job.

To calculate this, take your current household income and multiply it by 0.8. Then, divide your result by 12.

Formula to calculate target retirement savings by age

This formula recommends you save 25% of your gross salary each year, starting in your 20s. This includes your 401(k) holdings and matching contributions from your employer and other types of retirement savings.

If you follow this formula, it may allow you to accumulate your full annual salary by age 30. Continuing at the same average savings rate should yield the following:

- Age 35: two times annual salary

- Age 40: three times annual salary

- Age 45: four times annual salary

- Age 50: five times annual salary

- Age 55: six times annual salary

- Age 60: seven times annual salary

- Age 65: eight times annual salary

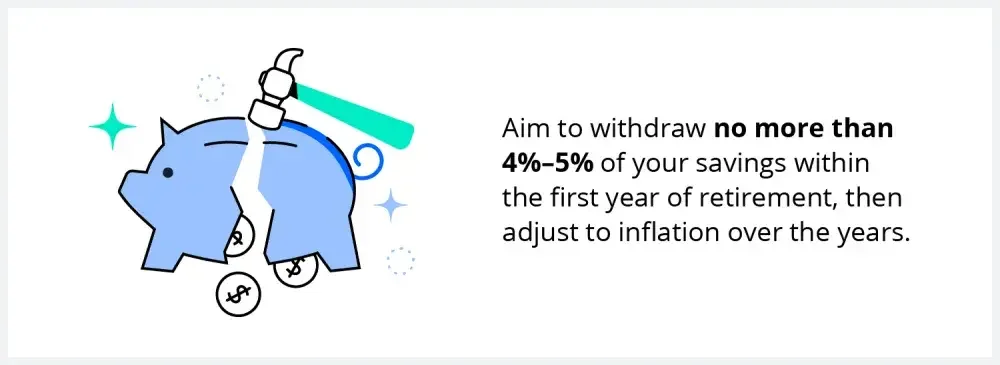

Calculation to help you determine how much to withdraw from retirement savings

Experts recommend using the 4% rule when coming up with how much you should withdraw from your retirement savings accounts.

To do this, calculate 4% of your total savings. This 4% is what you can withdraw within your first year of retirement. Then, account for inflation by adding 3% to your first-year figure. Every year, continue to add 3% more.

Formula to help you figure out your retirement budget

To find out what your budget in retirement looks like, use the 25x rule. With the 25x rule, you should have 25 times the amount you expect to spend in savings.

First, start with your current monthly budget. Next, multiply by 12 to get your rough budget for the year. Multiply that yearly budget by 25.

Additional retirement tips

There are many components to consider when it comes to retiring. To make the transition as smooth as possible, consider the additional retirement tips below:

Consider hiring a retirement adviser

Hiring a retirement adviser can be a great option if you're dealing with a more complex financial situation, such as needing more options to increase your retirement funds, receiving an inheritance from a family member, or just wanting extra help with financial planning.

Many experts also say that a good rule of thumb is to consider hiring an adviser when you can save 20% of your income at retirement age.

A financial adviser may not be worth it if:

- You don't need guidance managing your portfolio

- You aren't that close to retirement yet

- You can comfortably make your own investment decisions

- You aren't interested in complex financial strategies

Prepare for the unexpected

Before or during your retirement, prepare for unexpected expenses with a contingency plan. Sometimes, a medical expense or repair bill can come up, and you'll need to ensure you have the extra funds to cover those events.

Retirement planners usually recommend an emergency fund with six to 12 months' worth of expenses.

Look into long-term care insurance

Prepare for any expenses you'll need for long-term care with insurance. Long-term care insurance is there to cover services that aren't covered by Medicare and other regular health insurance, such as:

- Nursing home costs

- Assisted living facility costs

- Adult daycare centers

Purchasing this type of insurance can help add more protective barriers to your retirement savings and can provide more choices when it comes to health care. You may also consider giving someone health care power of attorney—they will be your representative to make decisions about your health care if something were to happen to you.

Create a retirement budget

Once you've calculated how much money you need for your retirement, create a budget to help you stay organized and on track with your spending. To create this budget, follow these steps:

- Start with your estimated retirement income calculation

- List your expected spending

- Consider any future spending/large purchases

- Factor in the costs of big lifestyle changes

- Set up a spending plan you can track and adjust

- Test your budget

Note: After setting up your budget, it's a good idea to test it out while you're still employed and before you're officially retired. That way, you still have a safety net if your budget needs readjusting.

Consult with a retirement attorney

To ensure the most official and secure retirement process, consult a retirement attorney. These professionals can help talk you through legal retirement documents and help you navigate the retirement process, including how to best take advantage of your assets and funds.

Once you've filled out the necessary legal documents, your attorney can help plan your retirement in a way that meets and protects your and your family's goals. These types of documents can include:

- Tax documents

- Account statements

- Retirement accounts

- Stock portfolios

- Estate planning

- Insurance policies

- Personal property

Note: The more information and documents you can provide your attorney, the easier the process will be.

Retirement resources

Check out these retirement resources for more information and guidance:

- AARP: Planning for Retirement

- Healthcare.gov

- Medicare.gov

- Veterans Benefits Administration

Retirement Checklist

Ready to take the plunge into retirement? View the checklist below to help you determine whether or not you're ready for retirement:

Transitioning into retirement

There's no one-size-fits-all answer to retirement, but you'll be prepared when your income, including your savings, Social Security, and any other sources, can support your lifestyle and needs while in retirement. Whether you want to travel the world or keep things simple while in retirement, connect with a LegalZoom financial adviser to guide you through the process.

'%20/%3e%3c/svg%3e)

'%3e%3cpath%20fill-rule='evenodd'%20clip-rule='evenodd'%20d='M9.31239%2025.5316H13.0679V14.1032H9.31239V25.5316ZM11.1913%208.46875C9.93945%208.46875%209%209.25086%209%2010.505C9%2011.5995%209.78211%2012.5389%2011.1913%2012.5389C12.6005%2012.5389%2013.3826%2011.5995%2013.3826%2010.505C13.3826%209.4082%2012.6005%208.46875%2011.1913%208.46875ZM27%2018.9577V25.5316H23.2445V19.4275C23.2445%2017.8609%2022.6174%2016.7664%2021.3679%2016.7664C20.2711%2016.7664%2019.644%2017.5463%2019.3316%2018.1756C19.1743%2018.488%2019.1743%2018.8004%2019.1743%2019.1128V25.5316H15.4165V13.9458H19.1743V15.5123C19.644%2014.7302%2020.5835%2013.6357%2022.6174%2013.6357C25.1234%2013.7908%2027%2015.3573%2027%2018.9577Z'%20fill='white'/%3e%3c/g%3e%3cdefs%3e%3cclipPath%20id='clip0_952_9489'%3e%3crect%20width='18'%20height='18'%20fill='white'%20transform='translate(9%208)'/%3e%3c/clipPath%3e%3c/defs%3e%3c/svg%3e)