Are you having trouble deciding how to protect what you’ve built and who it will go to? For many families, living trusts—popular tools in the estate planning process—offer a clear path forward. There are two kinds of living trusts: revocable and irrevocable. When deciding on the type of living trust that will work best for your particular circumstances, it’s essential to understand the differences between them. But when it comes to revocable vs. irrevocable trusts, the differences aren’t always obvious at first glance.

This article breaks down the essentials of revocable and irrevocable trusts, so you can understand what’s right for your needs.

Key takeaways

- A trust helps manage and distribute your assets and can help your estate avoid probate.

- A living trust is created during your lifetime and can be revocable (you can change or cancel it) or irrevocable (generally unchangeable after creation).

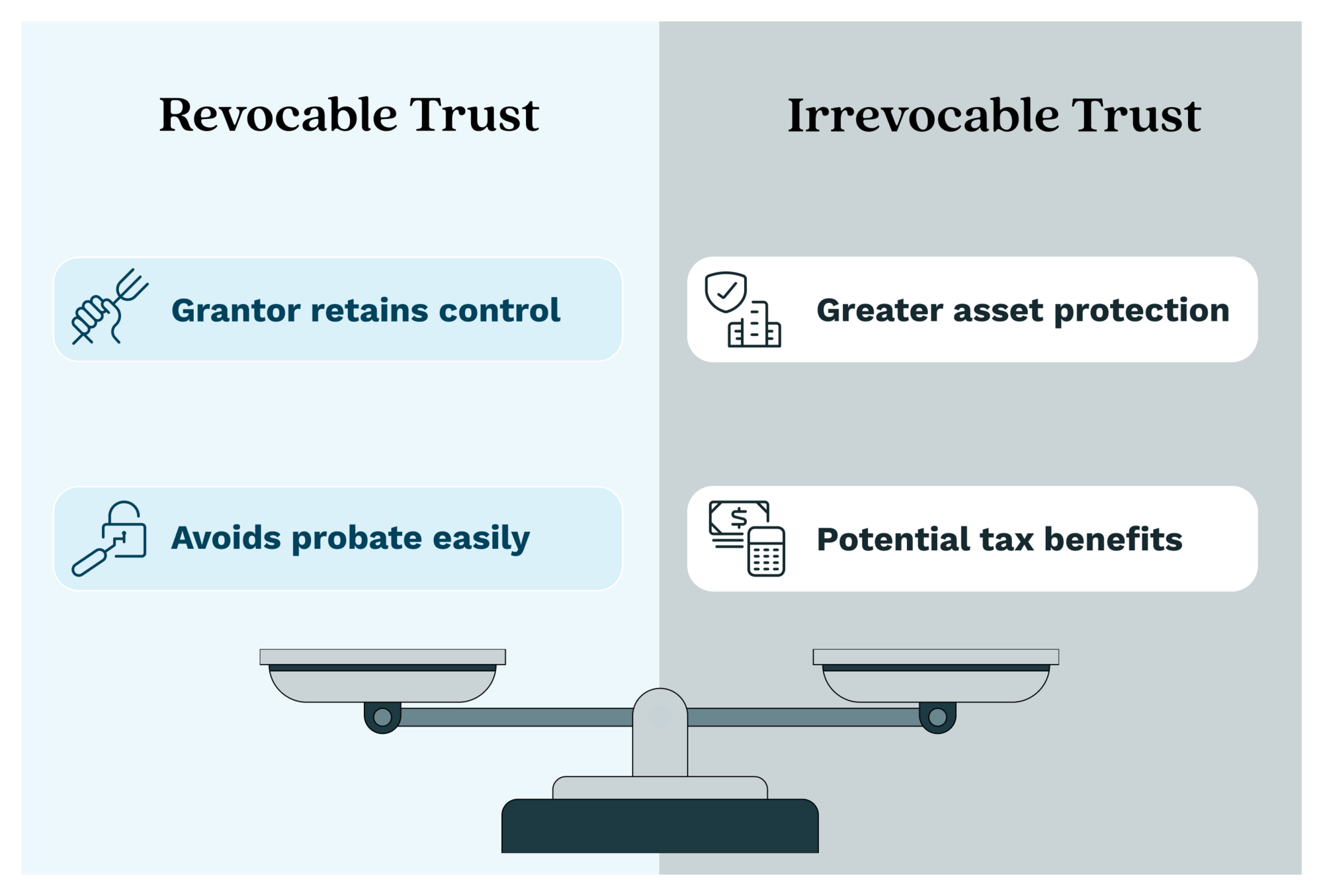

- Revocable trusts offer more control and flexibility, while irrevocable trusts provide stronger asset protection and potential tax advantages.

- Once the grantor dies, a revocable trust automatically becomes irrevocable, and the terms become unchangeable.

- Not all living trusts are revocable; some are intentionally established as irrevocable from the outset to meet specific planning needs.

- State laws can impact trust rules and tax treatment; therefore, it is essential to check your local regulations.

- It's wise to seek legal advice, as trusts can have significant tax and legal implications. LegalZoom offers convenient tools and attorney-assisted plans to simplify the process.

What is a living trust?

A living trust is a trust that you create during your lifetime. The purpose of a living trust is to hold your assets while you’re alive and distribute them according to your wishes after your death. As the trust owner, you can transfer all kinds of assets into your living trust, including real estate, bank accounts, family heirlooms, and more.

A living trust differs from a will in that it doesn't go through probate court. Therefore, the trust doesn’t become part of the public record.

A living trust can be revocable or irrevocable, with each having its own advantages.

What is a revocable trust?

A revocable trust is a living trust that you can revoke, amend, or cancel at any time. The revocable living trust is a comprehensive estate plan that allows you to retain control over your assets, even though the trust owns them. It offers you, as the grantor, the flexibility to make changes to it at any time.

However, once the grantor dies, the revocable trust automatically becomes an irrevocable trust, meaning the conditions cannot be altered or changed.

As the grantor of a revocable living trust, you can:

- Modify any of the trust terms

- Transfer assets in and out of the trust

- Reclaim property or spend money from the trust

- Change or remove your beneficiary, trustee, and successor trustees

- Revoke the trust at any time

What are the benefits of a revocable living trust?

- Avoiding probate. Because the trust owns the assets contained in the trust, these revocable trust assets aren't subject to the probate process upon your death. This means your assets are available for distribution, and your named beneficiaries can avoid the lengthy and often costly probate court process.

- Maximizing privacy. Assets that are part of the probate process are a matter of public record. By keeping your assets within the revocable trust, they will remain confidential.

- Planning your incapacitation. If you become unable to manage your affairs, whether due to illness, injury, or age, you can name a successor trustee to take over. This person will step in to manage your trust without needing court approval.

Revocable trust example

Sam is a father of two living in California. He wants to maintain control of his finances while ensuring his family won’t have to deal with court delays after he dies. He also values privacy and wants his personal assets to stay out of public records.

In Sam’s case, a revocable trust is a sensible option. It allows him to manage his own assets while he’s alive, make changes as needed, and pass everything on smoothly when the time comes. His heirs can avoid probate and access their inheritance faster. In this situation, it’s advisable for Sam to consider a revocable trust.

What does "rev tr" mean?

"Rev tr" is a common abbreviation for revocable trust. It can be changed, updated, or canceled by the person who created it (the grantor) during their lifetime.

What does RLT stand for in estate planning?

In estate planning, “RLT” stands for revocable living trust. The terms “revocable living trust” and “revocable trust” are often used interchangeably.

What are the disadvantages of revocable living trusts?

A revocable trust doesn’t offer asset protection. This means your assets in the trust are fair game for creditors, debt collectors, and plaintiffs in lawsuits. Furthermore, estate taxes apply to this type of legal entity. In other words, you can’t sidestep estate taxes with this option—all the assets held in the trust are still subject to state and federal estate taxes upon your death. You can also create revocable living trusts that help to reduce estate taxes, such as an AB trust for married couples.

Can you be the trustee of your own revocable trust?

Yes, many people designate themselves as trustees of their own revocable living trust. This allows them to maintain control until they die or become incapacitated.

What is an irrevocable trust?

An irrevocable trust also functions as its name indicates. It’s irrevocable, so once you’ve set it up, you can’t terminate, cancel, or make any changes to it.

Given its lack of flexibility, the irrevocable trust isn’t as popular within the estate planning process. Because it is irrevocable, once you transfer assets to the trust, you’ll no longer have control over them.

What are the benefits of an irrevocable living trust?

There are certain circumstances where an irrevocable trust might make sense, including the following situations:

- Minimization of estate taxes. Certain types of irrevocable trusts can help you reduce or eliminate estate taxes. In some cases, you can avoid estate taxes because your assets may not be considered part of your estate when you transfer them to the irrevocable trust. The rules for these trusts can be complex, so it’s always a good idea to consult with an estate planning attorney if your goal for your irrevocable trust is to minimize estate taxes.

- Medicaid eligibility. Government programs, such as Medicaid, often include specific thresholds that determine eligibility for the aid in question. By making your trust irrevocable, your beneficiaries are less likely to have their income or asset eligibility levels affected by the trust. However, the rules for Medicaid eligibility are complex and subject to frequent changes, so it is advisable to consult with a professional.

- Creditor and lawsuit protection. Because it can’t be terminated once it’s set up, the irrevocable trust offers more creditor protection to both the settlor of the trust and the trust’s beneficiaries than a revocable trust. This protection also applies to debt collectors and those who file lawsuits against the grantor, so if creditor protection is one of your objectives, consider an irrevocable trust.

- Avoiding probate court. Like revocable trusts, irrevocable trusts avoid probate, making it easier for your beneficiaries to receive your trust assets.

Irrevocable trust example

Alex lives in Texas and is planning ahead for future healthcare needs. He’s concerned about long-term care costs and wants to protect his home and savings from being counted when applying for Medicaid. He’s also not expecting to make any changes once his plan is in place.

Because of these goals, an irrevocable trust may be a better fit for Alex. By placing his assets in an irrevocable trust ahead of time, they may not be counted for Medicaid eligibility, and they could be shielded from lawsuits or creditors. Given his situation, Alex needs an irrevocable trust to protect his assets and qualify for benefits in the future.

What are the disadvantages of an irrevocable living trust?

While irrevocable trusts can offer asset protection, tax benefits, and aid in Medicaid planning, they also have certain downsides.

- Loss of control: Once the trust is created and funded, you give up ownership and control over those assets. That means you generally can’t sell, transfer, or use them without the trustee’s approval.

- Limited flexibility: Unlike revocable trusts, you can’t change beneficiaries or terms. This can be restrictive if your personal or financial situation changes.

- Complex setup and maintenance: Irrevocable trusts may require more legal guidance and ongoing administration by a qualified trust attorney, which can increase costs.

- Tax reporting requirements: These trusts may be taxed separately and may require a separate tax return, depending on their structure.

Understand the disadvantages of an irrevocable trust before determining whether the long-term benefits outweigh the limitations on control and access.

Can you be the trustee of your own irrevocable trust?

In most cases, you can’t be the trustee of your own irrevocable trust if your goal is to gain the typical tax advantages or creditor protection associated with it.

That’s because being both the grantor and trustee could mean you still have control over the trust, which defeats the purpose of making it legally separate from your estate. To qualify for protections, like exclusion from your taxable estate, or shielding assets from creditors or Medicaid rules, you need to appoint an independent trustee.

Therefore, if you’re considering creating an irrevocable living trust, relinquishing control as trustee is a key component of its effectiveness.

Comparison table: Revocable trust vs. irrevocable trust

If we’re comparing the two, a revocable trust tends to be less complicated and more straightforward than an irrevocable trust. The main differences are that revocable trusts provide more grantor control and flexibility, but offer no asset protection and limited estate tax benefits, while irrevocable trusts offer limited grantor control and flexibility, but provide more asset protection and potential tax advantages.

Here is a quick comparison table to clearly highlight the contrasting features.

| Feature | Revocable trust | Irrevocable trust |

|---|---|---|

| Control | You retain control; you can modify or cancel | Control is transferred to the trustee |

| Flexibility | High, you can amend the terms anytime | Low, changes require court or beneficiary approval |

| Asset protection | Limited protection from creditors or lawsuits | Stronger protection from creditors |

| Taxation | Income is taxed to the grantor | Trusts may be taxed separately, which can reduce estate taxes |

| Goes through probate? | No | No |

| Privacy | Maintains privacy after death | Maintains privacy after death |

| Best for | Flexibility, ongoing control | Estate tax planning, Medicaid eligibility |

How to choose the right trust for your needs

Living trusts are important estate planning tools, but understanding them can be difficult, so we advise speaking with an estate planning lawyer or estate planner for assistance. They can help you determine which kind of trust best suits your circumstances and introduce you to other estate planning tools. At LegalZoom, we offer convenient estate plan services.

When meeting with an estate planning professional to decide on the best course of action, you’ll need to consider your finances, businesses, and family structure, among other factors.

Finances

The amount of money you’ve and where that money is invested could impact your estate planning. For example, estates of a certain size are subject to the federal estate tax, so you would want to select a living trust that offers the best tax advantages. The complexity of your financial situation may also play a role in the decision.

Business

If you own a business, setting up a trust can help ensure your business stays intact. Your lawyer can help you determine which trust would most benefit the future of your business, protect it from certain creditors and lawsuits, and maximize tax exemptions.

Family

If you have a complex family structure, such as previous marriages or a blended family, you’ll need to take special care when choosing a trust and drafting your estate plan. You’ll want to choose a trust that provides the appropriate asset distribution for your chosen beneficiaries.

How to tell if a trust is revocable or irrevocable

Understanding your trust type is key to managing it correctly. But if you’re reviewing legal documents, here’s what to look for.

Step 1: Check the title of the document

Sometimes the trust name itself includes the words “revocable” or “irrevocable.” For example, “John Smith Revocable Living Trust.”

Step 2: Read the introductory clauses

Early in the trust document, look for language like “This trust is revocable by the grantor...” or “This trust shall be irrevocable upon execution.”

Step 3: Search for amendment clauses

If the document gives the grantor the power to change, amend, or cancel the trust, it’s revocable. If not, it’s likely irrevocable.

Step 4: Ask the drafting attorney

If you’re unsure, consult the estate planning attorney who created it. They can explain whether the trust is revocable or irrevocable and what that means for your rights.

State-specific trust rules and tax considerations

Below is an extended table summarizing key highlights for all 50 U.S. states, including revocable and irrevocable trusts, along with links to relevant government sites for validation. Where specific state-level details are not applicable, federal tax principles and general state trust law are referenced in the next table.

For the most up-to-date and detailed information, consult the official state government or revenue department site.

| State | Revocable trust highlights | Irrevocable trust highlights | Relevant government site |

|---|---|---|---|

| Alabama | Income from revocable trusts is taxed to the grantor; distributions to beneficiaries are taxed as income. | Irrevocable trusts are taxed as separate entities if income is retained; distributions are taxed to beneficiaries. | Alabama Dept. of Revenue |

| Alaska | Revocable trusts are taxed to the grantor; Alaska allows perpetual and self-settled trusts. | Non-grantor irrevocable trusts are taxed as separate entities; Alaska is a leading state for asset protection trusts. | Alaska Trust Act |

| Arizona | Revocable trusts are taxed to the grantor; used for probate avoidance. | Irrevocable trusts are taxed as separate entities; Arizona supports asset protection trusts. | Arizona Dept. of Revenue |

| Arkansas | Revocable trusts are taxed to the grantor; used for probate avoidance. | Irrevocable trusts are taxed as separate entities; Medicaid income trusts are allowed. | Arkansas Dept. of Finance |

| California | Transferring real estate into a revocable trust doesn't trigger reassessment under Prop 13 if you remain the sole beneficiary. | Transferring real estate property to an irrevocable trust for the benefit of the creator/grantor or their spouse is also exempt from reassessment. | Franchise Tax Board |

| Colorado | Revocable trusts are taxed to the grantor; probate avoidance. | Irrevocable trusts are taxed as separate entities; Colorado estate tax follows federal rules. | CO Dept. of Revenue |

| Connecticut | Revocable trusts are taxed to the grantor; probate avoidance. | Irrevocable trusts are taxed as separate entities; the estate tax applies based on exemptions. | CT Probate Court |

| Delaware | Revocable trusts are taxed to the grantor; Delaware is a leading trust jurisdiction. | Irrevocable trusts are taxed as separate entities, with strong asset protection laws. | Delaware Code Online |

| Florida | Assets in a revocable trust count for Medicaid eligibility. | An irrevocable asset protection trust can shelter the primary residence if it is funded at least 5 years before a Medicaid application. | Medicaid Planning Assistance |

| Illinois | Revocable trusts are taxed to the grantor; probate avoidance. | Irrevocable trusts are taxed as separate entities; Illinois imposes state income tax on trusts. | IL Tax |

| Maryland | Revocable trusts are taxed to the grantor; probate avoidance. | Irrevocable trusts are taxed as separate entities; the Maryland estate tax applies. | MD Comptroller |

| Massachusetts | Estate tax rules often prompt high-net-worth individuals to utilize irrevocable trusts for tax planning purposes. | Irrevocable trusts are recommended to minimize state estate tax and creditor exposure. | MA Estate Tax |

| Minnesota | Revocable trusts are taxed to the grantor; probate avoidance. | Irrevocable trusts are taxed as separate entities; the Minnesota estate tax applies. | MN Dept. of Revenue |

| Nevada | Revocable trusts are taxed to the grantor; probate avoidance. | Irrevocable trusts are taxed as separate entities; Nevada is a leading asset protection trust state. | NV State Laws |

| New Jersey | Revocable trusts are taxed to the grantor; probate avoidance. | Irrevocable trusts are taxed as separate entities; New Jersey estate tax was repealed in 2018. | NJ Dept. of Treasury |

| New York | Revocable trusts offer privacy but no protection from creditors or Medicaid. | Medicaid-qualifying irrevocable trusts can shelter assets and support long-term care planning. | NY Medicaid Trusts |

| Oregon | Revocable trusts are taxed to the grantor; probate avoidance. | Irrevocable trusts are taxed as separate entities; the Oregon estate tax applies. | OR Dept. of Revenue |

| Pennsylvania | Revocable trusts are taxed to the grantor; probate avoidance. | Irrevocable trusts are taxed as separate entities; the Pennsylvania inheritance tax applies to certain transfers. | Commonwealth of PA |

| Rhode Island | Revocable trusts are taxed to the grantor; probate avoidance. | Irrevocable trusts are taxed as separate entities; the Rhode Island estate tax applies. | RI Division of Taxation |

| South Dakota | Revocable trusts are taxed to the grantor; probate avoidance. | Irrevocable trusts are taxed as separate entities; South Dakota is a leading trust jurisdiction. | SD Dept. of Revenue |

| Texas | Revocable living trusts help avoid probate and simplify asset transfers. | Irrevocable trusts offer estate tax benefits and enhanced asset protection. | TX State Law Library |

| Washington | Revocable trusts are taxed to the grantor; probate avoidance. | Irrevocable trusts are taxed as separate entities; the Washington estate tax applies. | WA State Legislature |

| Wisconsin | Revocable living trusts avoid probate and allow the trustmaker's lifetime control. | Irrevocable trusts are favored for long-term care planning, as they offer stronger asset protection. | WI DHS |

| Wyoming | Revocable trusts are taxed to the grantor; probate avoidance. | Irrevocable trusts are taxed as separate entities; Wyoming is a leading trust jurisdiction. | WY Dept. of Revenue |

The following states follow federal rules.

| State | Revocable trust highlights | Irrevocable trust highlights | Relevant government site |

|---|---|---|---|

| Georgia, Hawaii, Idaho, Indiana, Iowa, Kansas, Kentucky, Louisiana, Maine, Michigan, Mississippi, Missouri, Montana, Nebraska, New Hampshire, New Mexico, North Carolina, North Dakota, Ohio, Oklahoma, South Carolina, Tennessee, Utah, Vermont, Virginia, West Virginia | Revocable trusts are taxed to the grantor; probate can be avoided. | Irrevocable trusts are taxed as separate entities; non-resident trusts may have special rules. | IRS.gov |

Summary

- General federal principles: In all states, revocable trusts are taxed to the grantor for income tax purposes; irrevocable trusts are taxed as separate entities unless distributions are made to beneficiaries, in which case the beneficiaries are taxed.

- State variations: Some states have unique asset protection trust statutes (e.g., Alaska, Nevada, South Dakota, Delaware, Wyoming). Others impose state estate or inheritance taxes (e.g., Massachusetts, Oregon, Minnesota, Washington, Rhode Island, Connecticut, New York, and New Jersey prior to 2018).

- Medicaid planning: Most states treat assets in revocable trusts as countable for Medicaid eligibility; irrevocable trusts may provide asset protection if properly structured and funded in advance of the look-back period.

For the most accurate and up-to-date information, consult the official state tax or revenue department linked above, or visit the IRS state government website list for direct access to all state resources.

Important trust terminologies

When drafting a living trust or an irrevocable trust, it’s essential to understand the language used in your trust agreement, especially if you’re managing substantial assets or planning for future generations.

- Non-revocable trust: A non-revocable living trust is simply another way to refer to an irrevocable trust, one that can’t be changed without court approval.

- Grantor / settlor / trustor: The legal owner and creator of the trust. In a revocable trust, the grantor retains control during their lifetime.

- Trustee: The person who makes decisions about the trust property and manages it in the best interests of the beneficiaries.

- Successor trustee: A successor trustee is an individual or an entity that steps in and takes over the functions of a trust if the original trustee is indisposed or is no longer able to fulfill their duties. This role is important in both revocable and irrevocable trusts. For revocable trusts, the successor typically takes over upon the grantor's incapacity or death. In irrevocable trusts, they may step in immediately if the grantor isn’t serving as trustee.

- Beneficiaries: Individuals or organizations that receive trust income or assets according to the trust’s terms.

- Estate tax: A federal (and sometimes state) tax on the value of an estate after death.

- Trust property: The assets held in the trust, which may include real estate, bank accounts, investments, or personal property.

- Creditor claims: Legal actions from creditors. An irrevocable trust may offer enhanced protection against creditor claims and legal judgments.

- Trust income: Earnings generated from trust-held assets, which may have their own tax reporting obligations, depending on the type of trust.

- Trust agreement: The legal document that outlines the purpose, rules, and structure of the trust.

- Legal process: Trusts may bypass probate but must still comply with applicable state laws.

Why choose LegalZoom for your trust

Whether you’re planning for substantial wealth, protecting a family business, or managing complex estate planning goals, LegalZoom makes it easy to start and stay on track.

At LegalZoom, we offer convenient estate plan services. You can set up your revocable or irrevocable trust in just a few simple steps and, depending on your selected plan, gain access to a qualified trust attorney who can answer your questions and provide tailored legal advice to meet your needs.

Here is what all happy customers say about our service:

"The process was fast, easy, and met my needs. The final product I received in the mail was spectacular! It exceeded my expectations!"

—Barbara F., living trust customer

FAQs about trusts

What’s the difference between a trust and a living trust?

A trust is a legal arrangement in which one party (the grantor) grants another party (the trustee) the right to hold and manage assets on behalf of the beneficiaries. Trusts are often used to simplify asset transfers, avoid probate, and protect privacy.

So when comparing a trust vs living trust, the difference lies in timing and purpose. A living trust is established during your lifetime to help you manage your assets now and pass them on without the need for probate. In contrast, the term “trust” can also refer to other types, such as revocable trusts, irrevocable trusts, or trusts that only take effect after the death of the grantor.

In short, all living trusts are trusts, but not all trusts are living trusts.

What assets can be placed in an irrevocable trust?

You can transfer real estate, investments, business interests, and life insurance policies into an irrevocable trust fund.

Can you sell assets in an irrevocable trust?

Yes, but only the trustee can do so, and only if the trust allows it and the action benefits all the beneficiaries.

Does an irrevocable trust protect assets from creditors?

In many cases, yes. An irrevocable trust may shield assets from creditor claims, legal judgments, and some forms of liability.

What happens to a revocable trust after the grantor dies?

When a grantor dies, the revocable trust becomes an irrevocable trust, and the successor trustee appointed in the trust document will provide continuous management of the trust.

Do revocable trusts protect assets from creditors?

No, a revocable trust does not protect its assets from creditors, debt collectors, or plaintiffs in lawsuits. This means creditors can collect from revocable trusts.

Do irrevocable trusts have to pay estate taxes?

Not always. One of the main benefits of an irrevocable trust is that the assets placed in it are often excluded from your taxable estate, which can reduce or eliminate estate taxes. This works because the assets are no longer considered yours for tax purposes, but it depends on how the trust is structured and current tax laws.

Can I modify an irrevocable trust?

The whole purpose of an irrevocable trust is to limit changes. Although irrevocable trusts are not designed for modification, there are ways to make changes. Typically, any change requires all parties to agree on it and submit a consent modification document or trust amendment. However, in other cases, you may be able to request changes through the court.

Is a family trust revocable or irrevocable?

It can be either. A family revocable trust refers to a trust created during your lifetime that benefits family members and remains changeable while you're alive. Alternatively, a family irrevocable trust is created to hold and manage assets for the benefit of family members (beneficiaries), which can’t be modified after.

What is the difference between Inter vivos trusts and revocable trusts?

Inter vivos trusts, also known as living trusts, are created while you're alive, much like a living trust. These can be revocable or irrevocable, depending on how you draft them.

What is a grantor trust vs. a revocable trust?

A grantor trust is a type of trust in which the person who creates it, the grantor, retains certain powers or control, such as the right to modify the trust or benefit from its income. For tax purposes, the IRS treats the trust’s income as if it still belongs to the grantor.

When comparing a grantor trust to a revocable trust, it is helpful to know that many revocable trusts also function as grantor trusts, as the grantor retains control over the trust. However, not all grantor trusts are revocable; a grantor trust can also be irrevocable, depending on its setup.

For example, a revocable grantor trust allows the grantor to retain full control and make changes during their lifetime, while an irrevocable grantor trust still treats the grantor as the owner for tax purposes but limits their ability to modify or access the trust’s assets. The key difference lies in who controls the trust and how flexible it is, even though the grantor is still taxed on the income in both cases.

Can an irrevocable trust be converted to a revocable trust?

No, you can't change an irrevocable trust to a revocable trust. The primary purpose of creating an irrevocable trust is to ensure it remains unmodifiable, thereby qualifying for tax and credit exemptions. So, if someone wishes for a different structure, they would need to terminate the original trust (if permitted) and establish a new revocable trust instead.

Can a grantor withdraw money from an irrevocable trust?

Only if the terms or state law allow it. In most cases, once assets are placed in an irrevocable trust, the grantor relinquishes direct access to the funds. However, some irrevocable trust agreements include limited rights for the grantor or allow for distributions under specific conditions.

Can you add assets to an irrevocable trust?

Yes, though you must follow the trust’s guidelines. The trust agreement will typically specify whether you can add new assets and under what conditions. Adding assets to an irrevocable trust may have tax or legal implications, so it’s best to do so with professional guidance.

Can beneficiaries be changed in an irrevocable trust?

Usually, no, unless powers of appointment exist or a court approves the change. In most irrevocable trusts, the list of beneficiaries is set once you establish the trust. That said, some irrevocable trusts grant specific individuals (often the grantor or trustee) the right to modify who receives the assets.

Can you have more than one irrevocable trust?

Yes. There’s no legal limit to the number of irrevocable trusts you can set up. People sometimes create multiple trusts to manage different assets, serve different beneficiaries, or achieve specific estate planning objectives. But whether you should have more than one depends on your personal situation. In many cases, a well-structured irrevocable trust is sufficient, but for more complex estates, multiple trusts may offer better flexibility and tax planning options.

Chloe Packard and Belle Wong, J.D., contributed to this article.

'%20/%3e%3c/svg%3e)

'%3e%3cpath%20fill-rule='evenodd'%20clip-rule='evenodd'%20d='M9.31239%2025.5316H13.0679V14.1032H9.31239V25.5316ZM11.1913%208.46875C9.93945%208.46875%209%209.25086%209%2010.505C9%2011.5995%209.78211%2012.5389%2011.1913%2012.5389C12.6005%2012.5389%2013.3826%2011.5995%2013.3826%2010.505C13.3826%209.4082%2012.6005%208.46875%2011.1913%208.46875ZM27%2018.9577V25.5316H23.2445V19.4275C23.2445%2017.8609%2022.6174%2016.7664%2021.3679%2016.7664C20.2711%2016.7664%2019.644%2017.5463%2019.3316%2018.1756C19.1743%2018.488%2019.1743%2018.8004%2019.1743%2019.1128V25.5316H15.4165V13.9458H19.1743V15.5123C19.644%2014.7302%2020.5835%2013.6357%2022.6174%2013.6357C25.1234%2013.7908%2027%2015.3573%2027%2018.9577Z'%20fill='white'/%3e%3c/g%3e%3cdefs%3e%3cclipPath%20id='clip0_952_9489'%3e%3crect%20width='18'%20height='18'%20fill='white'%20transform='translate(9%208)'/%3e%3c/clipPath%3e%3c/defs%3e%3c/svg%3e)