A corporation is a legal business entity that is separate from its owners, which can protect you from any business liabilities and help get your business off the ground.

Whether it's to save money on taxes, attract investors, protect yourself, or boost reputability, starting a corporation might be the best next step for you and the business.

Scope: This guide covers standard for-profit business corporations only, not nonprofits, professional corporations, or benefit corporations. The U.S. Small Business Administration provides additional context on choosing between entity types.

Steps to form a corporation: a quick overview

- Decide if a corporation is the right structure

- Choose your state of incorporation

- Name your corporation and check availability

- Appoint a registered agent

- Prepare and file your articles or certificate of incorporation

- Adopt bylaws and hold your organizational meeting

- Issue stock and set up ownership records

- Get an employer identification number (EIN) from the IRS

- Open a business bank account and register for state taxes

- Meet ongoing compliance requirements

What is a corporation, and is it the right structure for you?

A corporation is a legal entity that exists independently of its owners. It can sign contracts, own property, take on debt, sue, and be sued in its own name.

Owners (shareholders) hold equity through shares of stock. A board of directors sets strategy. Officers handle daily operations. These three layers form the governance structure.

Because the corporation is a separate entity, shareholders generally aren't personally responsible for its debts or legal judgments. Creditors typically can't reach shareholders' personal assets.

That protection isn't unconditional. Courts can pierce the corporate veil if corporate formalities were ignored, personal and business finances were commingled, or the corporation was used for fraud.

Beyond liability protection, corporations can issue multiple classes of stock. That makes them the preferred structure for raising outside investment, attracting venture capital, or going public. The tradeoff is that corporations have more formalities than other structures, including annual meetings, board resolutions, separate financial records, and state compliance filings.

Corporation vs. LLC: a quick comparison

An LLC also provides limited liability, so that alone doesn't distinguish the two. The real differences: governance structure, fundraising flexibility, and default tax treatment.

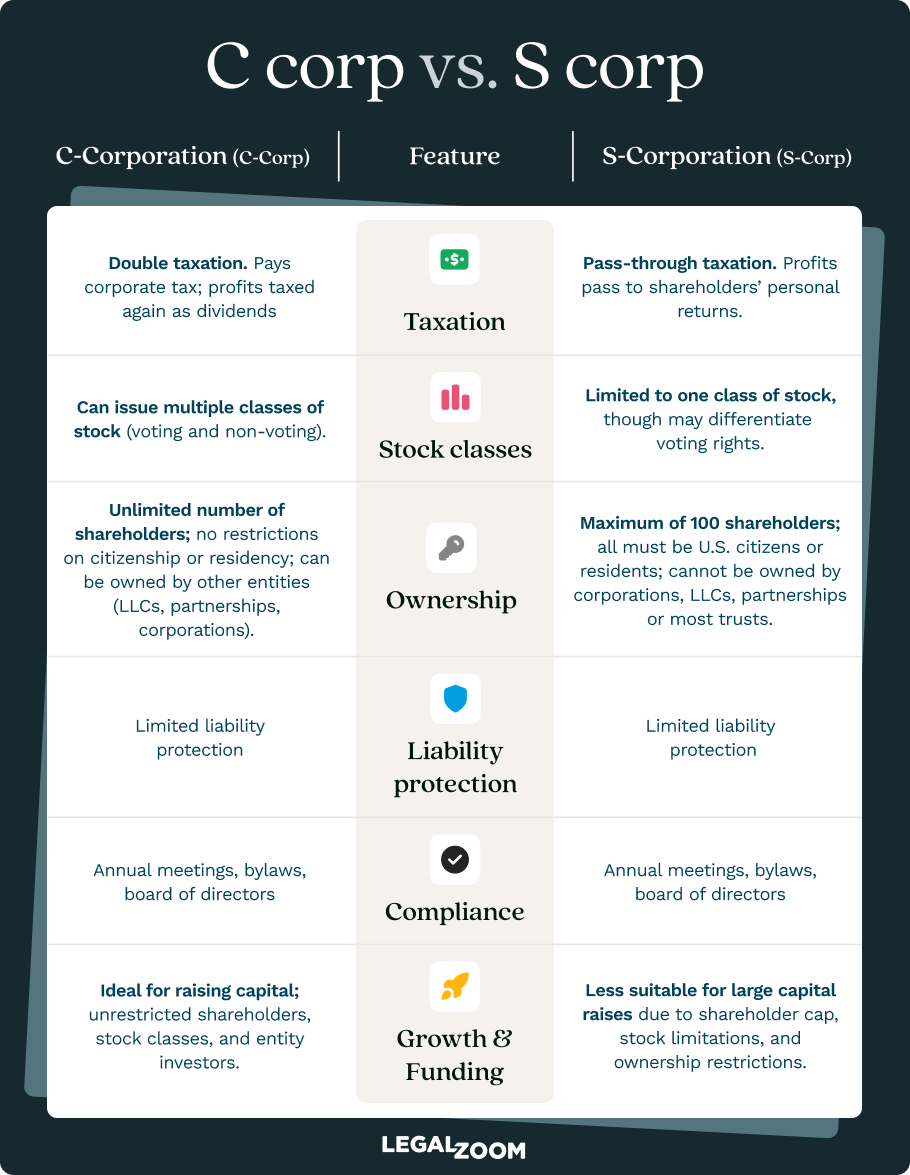

C corporation vs. S corporation

When you file formation documents with a state, you create a corporation. There's no C corp or S corp box on the state form.

A C corporation is the default federal tax classification. C corps pay tax at the corporate level on profits, and shareholders also pay tax on dividends. This is commonly called double taxation.

An S corporation is a tax election, not a separate entity type. You make it with the IRS using Form 2553. Read our comparison of S corp vs. LLC for more context.

If approved, income, losses, deductions, and credits pass through to shareholders' personal returns, bypassing double taxation.

All shareholders must sign the form. You always form a standard corporation at the state level first, then make the federal election separately.

IRS eligibility for S corp status:

- No more than 100 shareholders

- Shareholders must be U.S. citizens, permanent residents, or resident aliens. Only one class of stock; shareholders must be individuals, estates, or certain trusts.

- Must be a domestic U.S. entity, and certain types like insurance companies may be ineligible

Filing deadline: Form 2553 must be filed within two months and 15 days of the beginning of the tax year in which the election takes effect. For a calendar-year corporation wanting S corp treatment for 2027, the deadline is March 15, 2027.

Form 2553 must be mailed or faxed; there's no online option. Confirm the exact deadline with a tax professional.

| Consider staying a C corp if... | Consider an S corp election if... |

|---|---|

| You plan to raise venture capital or institutional investment | Pass-through taxation—profits reported on personal tax returns without business-level taxation |

| You want multiple classes of stock | You want pass-through taxation to avoid double taxation |

| You have non-U.S. shareholders | You meet IRS eligibility rules (100 or fewer shareholders, one class of stock, eligible shareholders only) |

| You may eventually go public | You are not planning to seek institutional investments |

Where should you incorporate?

You file in one state, and that choice affects your costs, administrative burden, and compliance obligations.

The general rule: If you'll primarily operate in one state, incorporate there. You avoid fees, paperwork, and compliance obligations from maintaining registrations in two states.

The Delaware question

Incorporating in Delaware has its advantages, and for some companies, the pitch is legitimate. Its corporate law is well-developed, extensively litigated, and familiar to investors and lenders. Over two-thirds of Fortune 500 companies are incorporated there.

That makes it a sound choice for startups raising outside capital or businesses with complex equity structures. For a detailed walkthrough, see our guide on how to form a Delaware corporation.

Every for-profit Delaware corporation must file an annual franchise tax report and pay franchise tax by March 1. This applies even if the corporation does no business in Delaware or earns no income there.

Delaware isn't automatically right for every business. If you incorporate in Delaware but primarily operate in California, you'll almost certainly need to register as a foreign corporation there too. That means paying fees and meeting compliance obligations in both states.

The two-state trap: understanding foreign qualification

Foreign qualification means registering your corporation to do business in a state other than where it was formed. It adds costs: two registered agents, two sets of annual reports, two filing deadlines, and two fee schedules.

Penalties for operating without qualifying vary by state but commonly include fines and the inability to bring lawsuits in state courts until the corporation qualifies.

Note: What counts as "doing business" in a state isn't straightforward. Most statutes list activities that don't qualify (like having a bank account or engaging in interstate commerce) rather than defining what does. If you're unsure, consult a business attorney.

Nevada, Wyoming, and other frequently marketed states

Nevada and Wyoming are marketed for privacy provisions and tax advantages. Whether those benefits apply depends on where you actually operate.

A Nevada corporation doing business in California still needs to foreign qualify there, paying fees and filing in both states. For most small, closely held businesses, incorporating in your home state is the most practical path.

How to form a corporation: step-by-step guide

You’ll follow four main steps: choose a name, appoint a registered agent, prepare and file your formation documents, and pay the filing fee. Once the state accepts your filing, the corporation legally exists.

Step 1: Choose and check your corporation name

Your name must be distinguishable from all other registered business names in your state. Even minor differences like punctuation or a plural form may not be enough. Run a name availability search through your state's Secretary of State website before you draft anything.

- Corporate designators are required. Most states require a word or abbreviation signaling corporate status: Corporation, Corp., Incorporated, Inc., Company, Co., Limited, or Ltd. Check your state's rules.

- Some words need special approval or are prohibited. Words like “bank,” “insurance,” “trust,” “university,” and “federal” are frequently restricted. Verify restricted word lists with your Secretary of State.

- Name reservation holds your name while you prepare. Most states let you reserve a name for 30 to 120 days for a small fee.

- State name approval isn't trademark clearance. Clearing the state database only means no other registered business in that state uses the same name. A name that clears there can still conflict with an existing federal trademark, exposing you to potential infringement claims. Search the USPTO's trademark database before committing.

Step 2: Appoint a registered agent

A registered agent (also called a statutory agent or agent for service of process) receives official legal and government documents on your corporation's behalf: lawsuit notices, compliance notices, and tax correspondence. Most U.S. corporations must have one.

Two requirements apply in most states: the agent must have a physical street address (not a P.O. box) in the state of incorporation and must be available at that address during business hours.

Your options:

- Serve as your own agent. Most states allow you to act as an agent if you are a resident of the state with a physical in-state address and are reliably available during business hours. Your address will appear in the public record.

- Use a registered agent service. These generally run $100 to $300 per year. A service keeps your personal address off public filings and is necessary if you incorporate out of state. LegalZoom's registered agent service handles this for you.

If your registered agent changes after filing, you must notify the state through a formal filing, which typically carries a fee.

Step 3: Prepare your formation documents

The document that creates your corporation varies by jurisdiction. Most states call it articles of incorporation, though you may also see certificate of incorporation, certificate of formation, and similar names used.

Gather all information below before opening the state's filing portal. Incomplete submissions are the most common cause of deficiency notices and delays.

| Field | What the state is asking for |

|---|---|

| Corporation name | Your confirmed, available name, including the required corporate designator |

| Registered agent | Legal name and physical in-state street address |

| Principal business address | Where the corporation conducts business; P.O. boxes generally are not accepted |

| Purpose clause | What the corporation is formed to do; most states accept a general clause covering all lawful business |

| Authorized shares | Maximum number of shares the corporation can issue |

| Share class information | Required only if you plan more than one class of stock |

| Incorporator name or signature | The person who executes and submits the filing; doesn't need to be a future officer or shareholder |

| Initial directors | Some states require this; others don't |

| Effective date | Most filings take effect on acceptance; some states allow a future date |

Understanding authorized shares. Authorized shares are the ceiling: the maximum shares the corporation can legally issue. A corporation with 100,000 authorized shares may issue only 10,000 to founders and leave the remaining shares unissued for future grants, option pools, or investor rounds.

Step 4: File with the state and pay the filing fee

Submit your completed formation documents to the appropriate state office (typically the Secretary of State or Division of Corporations). Online filing is generally faster and less error-prone than mail.

- Filing fee. Fees commonly fall in the $50 to $300 range, though some states calculate them based on authorized shares. Verify the current fee with your Secretary of State before submitting.

- Processing time. Standard processing ranges from same-day in some states to several weeks in others. Most states offer expedited options for an additional fee.

When the corporation legally exists. Your corporation exists when the state accepts the filing, not when you submit it. Errors or missing information trigger a deficiency notice, adding days or weeks.

When the state approves your filing, you'll receive a stamped or certified copy. Keep this permanently. You may need it to open a bank account, for investor due diligence, and as legal proof of your corporation's existence.

Certified copies and certificates of good standing are available from the state for an additional fee. Banks frequently require a certified copy to open a corporate account. Order one at the time of filing or right after approval.

What to do in the first 30 days after approval

State approval creates your corporation as a legal entity. It doesn't make it operational. Legally forming a corporation is only part of the process—post-formation steps matter equally.

1. Hold your organizational meeting and adopt bylaws

The organizational meeting is the corporation's first formal action after state approval. It's typically conducted by the initial directors or, if none have been appointed, the incorporator.

At this meeting, the corporation should:

- Adopt bylaws. These are the internal rules governing how the corporation operates—meeting procedures, voting requirements, officer roles, and quorum rules. Operating without them creates governance ambiguity and raises red flags during due diligence. Learn more about maintaining your corporate veil.

- Appoint or confirm the board of directors and elect officers. Officers typically include a President or CEO, Secretary, and Treasurer or CFO; titles vary by state. See our guide on appointing corporate officers.

- Authorize stock issuance. Assign stocks to founders and initial shareholders.

- Authorize opening a business bank account. Most banks require a corporate resolution from this meeting.

- Address other foundational matters. Can be approving a fiscal year, ratifying pre-formation contracts, or anything else that matters to your business.

Many states allow a written consent in lieu of a meeting for single-founder corporations, so double-check your state's rules. All decisions must be documented in minutes or a written consent and kept in the corporate records book.

2. Issue stock and set up your ownership records

Stock issuance establishes legal ownership in the corporation. Shares should be issued promptly after formation to clearly document who owns what portion of the company. In some cases, founders may have agreed ownership interests before issuance, but those interests should be formally reflected in the corporation’s stock records as soon as possible.

- Decide the share allocation. Determine how many shares each founder will receive out of the total authorized shares.

- Document the consideration. Each shareholder must contribute something of value, which could be cash, property, or services. Some states restrict stock issued for future services.

- Prepare stock certificates or equivalent records. Many modern corporations issue uncertificated shares, but the issuance must be formally documented either way.

- Record the issuance in a stock ledger. This is your cap table: who owns shares, when issued, at what price, and any transfers. Keep it current; it will be scrutinized in any fundraising round or legal dispute.

If you're issuing shares to multiple founders with different ownership percentages, or if shares are subject to vesting, consult a business attorney first. Mistakes in the ownership structure at formation are expensive to fix later.

A note on securities law: For most small, closely held corporations issuing founder shares, a federal exemption under Section 4(a)(2) of the Securities Act typically applies. Founders with complex equity structures should confirm the applicable exemption with a securities attorney.

3. Get your EIN, open a bank account, and register for taxes

You can apply for an EIN directly through the IRS. The IRS issues the EIN immediately at no cost. Learn which business entities need an EIN.

Then, open a dedicated bank account in the corporation's name once you have your EIN and state-approved formation documents. Most banks also require a corporate resolution authorizing the account. Keeping personal and business finances completely separate is one of the most direct ways to preserve the corporate veil.

Commingling funds is one of the strongest predictors of courts piercing the corporate veil.

You may need to register for state income tax withholding, sales tax collection, unemployment insurance, or other accounts. Check your state's Department of Revenue for the registrations that apply.

S corp election timing: Form 2553 must be filed no more than two months and 15 days after the beginning of the tax year the election takes effect, or any time during the preceding tax year. For a calendar-year corporation wanting S corp treatment for 2026, the deadline is March 16, 2026 (March 15 falls on a Sunday).

Missing this window means waiting until the following tax year. Confirm your specific deadline with a tax professional.

How much does it cost to form a corporation?

The state filing fee is only one piece of the cost when you form a corporation. The gap between one-time formation costs and recurring annual costs surprises founders who budgeted only for the initial filing.

| Cost item | Typical range | Notes |

|---|---|---|

| State filing fee | $50 to $300+ | Varies by state; some tie fees to authorized shares |

| Name reservation fee | $10 to $50 | Optional; only if you want to hold the name before filing |

| Registered agent services | $100 to $300/year | Required if using a service; free if you serve yourself |

| Expedited filing fees | Varies | Optional; available in most states |

| Certified copy or certificate of good standing | $10 to $50 | Some banks require it to open a bank account; required for foreign qualification |

| Annual report fee | $25 to $500+ | Required in most states; deadlines and amounts vary |

| Franchise tax | Varies widely | Some states charge this regardless of profitability |

| Business bank account | Usually free to open | Some banks charge monthly maintenance fees |

DIY, formation service, or attorney: Which path is right for you?

| Path | Best For | What gets handled | Main risks |

|---|---|---|---|

| DIY filing | Simple corporation, single-owner, paperwork-comfortable founder | You handle everything directly with the state and the IRS | Missed steps, filing errors, wrong state or entity choice |

| Formation service | Founder wants convenience without full custom legal work | Service prepares and files state formation docs; may offer add-ons like registered agent, EIN assistance, compliance reminders | False sense that formation is complete once filing is approved |

| Attorney-led formation | Multiple founders, investor plans, custom equity, regulated business, foreign owners | Legal strategy, custom docs, share structure guidance, founder agreements, filing oversight | Higher cost, but best protection against structural mistakes |

FAQs about forming a corporation

Do I need a lawyer to form a corporation?

No law requires it. Many founders of a corporation file directly with their state or use a formation service. For a single-owner corporation with a simple structure, that's workable.

How long does it take to form a corporation?

It varies widely. Some states process online filings within one business day. Delaware can process a filing in as little as one hour with paid expedited options.

Standard mail-in filings in some states take several weeks. A deficiency notice resets the clock, so filing accurate documents is the most reliable way to avoid delays. Check current processing times on your state's Secretary of State website.

What is the difference between articles of incorporation and corporate bylaws?

Articles of incorporation is the state-filed document that legally creates the corporation. It's public record. Bylaws are the internal governance rules adopted after formation: how meetings are held, how directors are elected and removed, what constitutes a quorum, and how bylaws can be amended.

Can one person form and own a corporation?

Yes. Most states allow a single individual to serve as sole shareholder, sole director, and one or more officers. The same formalities apply.

A sole owner who skips formalities faces the same veil-piercing risk as a multi-owner corporation. Courts look at whether formalities were observed, not how many shareholders were involved.

What is a registered agent, and do I need one?

A registered agent is a person or company designated to receive legal and government documents on behalf of your corporation. Every state requires one with a physical street address in the state of incorporation. You can serve yourself if you have a qualifying address and are consistently available during business hours, or use a professional service.

Failing to maintain one can result in default judgments entered against your corporation without your knowledge.

What happens if I miss my annual report deadline?

Most states impose late fees immediately. LegalZoom's business compliance services can help you track deadlines.

Extended non-filing results in loss of good standing, which can block lawsuits, financing rounds, and bank accounts. Continued non-filing leads to administrative dissolution.

Reinstatement requires filing all past-due reports, paying accumulated late fees, and submitting a reinstatement application. If another entity claimed your name during dissolution, you may need a new one.

Is forming a corporation in Delaware always the best choice?

Delaware has advantages, but it’s not necessarily the best state to incorporate for everyone. Delaware's Court of Chancery produces deep, predictable corporate legal precedent, and institutional investors are broadly familiar with its General Corporation Law. That makes Delaware a strong default for venture-backed startups or companies issuing complex stock—incorporations there grew roughly 30% in 2025.

But for a small, closely held business operating in one state, those advantages rarely justify the added formation and compliance costs.

Does the name I register with the state protect it as a trademark?

No. State name approval only confirms the name is distinguishable from other registered businesses in that state. It provides no trademark protection.

Search the USPTO trademark database for federal conflicts before committing.

When should I file Form 2553?

Form 2553 must be filed no more than two months and 15 days after the beginning of the tax year the election takes effect, or any time during the preceding tax year. You must mail or fax it; the IRS doesn't accept it online. Missing the deadline defaults your corporation to C corp treatment for that year.

Late election relief exists but isn't guaranteed. Confirm the exact deadline with a tax professional.

'%20/%3e%3c/svg%3e)

'%3e%3cpath%20fill-rule='evenodd'%20clip-rule='evenodd'%20d='M9.31239%2025.5316H13.0679V14.1032H9.31239V25.5316ZM11.1913%208.46875C9.93945%208.46875%209%209.25086%209%2010.505C9%2011.5995%209.78211%2012.5389%2011.1913%2012.5389C12.6005%2012.5389%2013.3826%2011.5995%2013.3826%2010.505C13.3826%209.4082%2012.6005%208.46875%2011.1913%208.46875ZM27%2018.9577V25.5316H23.2445V19.4275C23.2445%2017.8609%2022.6174%2016.7664%2021.3679%2016.7664C20.2711%2016.7664%2019.644%2017.5463%2019.3316%2018.1756C19.1743%2018.488%2019.1743%2018.8004%2019.1743%2019.1128V25.5316H15.4165V13.9458H19.1743V15.5123C19.644%2014.7302%2020.5835%2013.6357%2022.6174%2013.6357C25.1234%2013.7908%2027%2015.3573%2027%2018.9577Z'%20fill='white'/%3e%3c/g%3e%3cdefs%3e%3cclipPath%20id='clip0_952_9489'%3e%3crect%20width='18'%20height='18'%20fill='white'%20transform='translate(9%208)'/%3e%3c/clipPath%3e%3c/defs%3e%3c/svg%3e)