Decanting a trust can be compared to the process of transferring a fine wine into a new bottle, leaving behind unwanted sediment. In estate planning, the same principle applies. When an existing trust becomes outdated, restrictive, or contains provisions that no longer meet the needs of the grantor or beneficiaries, a trustee may “decant” the trust by moving its assets into a newly created trust with updated terms.

Trust decanting is the legal process of transferring assets from one trust into a newly created one while discarding provisions that no longer serve the best interests of the grantor or the beneficiaries. It gives trustees a way to modernize irrevocable trusts, which are often too rigid to amend through traditional means. Here are the key reasons trust decanting matters:

- Flexibility. Decanting provides trustees with a means to adapt a rigid, irrevocable document to present-day needs without starting from scratch.

- Modernization. Many older trusts don’t account for digital assets, evolving tax laws, or today’s fiduciary standards. Decanting helps bridge that gap.

- Beneficiary protection. Decanting can clarify distributions, strengthen spendthrift protections, preserve government benefit eligibility for individuals with special needs, or enhance asset protection in favorable jurisdictions.

What is trust decanting, and how does it work?

At its core, trust decanting is a method for updating an otherwise rigid, irrevocable trust. The process involves transferring the assets of an existing trust into a new trust that contains updated or improved terms.

This strategy has become more common in estate planning as families and trustees face changing tax laws, evolving family circumstances, and the need for greater flexibility. Many older trusts were drafted decades ago, and provisions that once made sense may now cause problems. Decanting provides a practical solution for modernizing those trusts.

How is decanting different from amending a trust?

It is important to distinguish decanting an irrevocable trust from simply amending a trust. Most irrevocable trusts cannot be amended directly, since their terms are intended to remain fixed once created.

- Amending a trust changes the original trust instrument itself.

- Decanting a trust transfers assets from the old trust into a new trust that contains updated provisions.

In other words, decanting creates a modernized version of the trust that better meets the needs of the grantor and beneficiaries. This approach provided trustees with a means to modify an irrevocable trust when direct amendment isn’t possible.

But it is very important to understand that decanting is not an unrestricted power. In most jurisdictions, a trustee cannot eliminate a beneficiary’s vested right to receive property, reduce a fixed income interest or mandatory distribution right, or unreasonably increase their own trustee compensation or reduce their liability standard.

Why consider decanting a trust?

Trustees may consider decanting when the original trust no longer serves its intended purpose or creates administrative challenges. The purpose of decanting a trust is to keep an irrevocable trust effective and relevant while still honoring the grantor’s intent.

Below are the primary reasons trustees choose to decant a trust, along with practical illustrations:

1. Correcting drafting errors or ambiguities

Even well-drafted trusts can contain unclear or outdated language. Ambiguous provisions may lead to confusion, disputes, or even litigation among beneficiaries. Decanting allows trustees to transfer assets into a new trust with clearer language, thereby reducing the risk of future conflicts. For example, if a trust vaguely defines “income” or “principal,” a decanted trust can clarify those definitions to ensure consistent interpretation.

2. Adapting to changes in tax or property law

State and federal tax laws evolve frequently, and a trust created decades ago may no longer align with today’s tax environment. Decanting provides trustees with an opportunity to update the trust’s terms, which ensures that beneficiaries don’t miss out on tax savings or encounter compliance issues. For example, a trust established before the 2017 Tax Cuts and Jobs Act might need to be decanted to reflect current estate and gift tax exemptions.

3. Updating trustee powers or succession provisions

Some older trusts restrict trustee powers in ways that make administration inefficient today. Others may not clearly outline how a successor trustee should be chosen if the original trustee resigns, becomes incapacitated, or passes away. Through decanting, trustees can expand their powers, such as allowing investment in modern asset classes or setting out a smoother process for trustee succession.

4. Enhancing beneficiary protection

Decanting is often used to strengthen protections for vulnerable beneficiaries. For instance, a trust can be decanted to include special needs provisions that preserve government benefit eligibility for a beneficiary with disabilities. Similarly, it can enhance spendthrift protections, preventing creditors or ex-spouses from gaining access to a beneficiary’s inheritance.

5. Modifying distribution terms

Life circumstances change, and the original distribution plan in a trust may no longer fit a family’s needs. Trustees can use decanting to alter when and how distributions occur. For example, if a beneficiary develops a gambling addiction in his early twenties, then instead of requiring outright distributions at age 25, a decanted trust could allow staggered payments at ages 30, 35, and 40, thereby providing more long-term security.

6. Simplifying administration

Sometimes, administering multiple small trusts can be burdensome, or one trust may become too complicated for efficient management. Decanting can consolidate several trusts into one, which reduces costs and administrative work. In other cases, decanting may result in the splitting of a trust into two or more separate trusts, such as when siblings have different financial needs or risk profiles.

How do state laws affect trust decanting?

State laws play a crucial role in determining whether and how a trustee can decant a trust. Since trust law is primarily governed at the state level, the availability, scope, and limitations of decanting can vary significantly by jurisdiction, and you should speak to an estate planning attorney. These differences directly affect both the process and the degree of flexibility a trustee has when modifying an irrevocable trust.

Uniform Trust Decanting Act (UTDA)

The Uniform Trust Decanting Act is a model law developed to promote consistency in decanting rules across jurisdictions. It provides a structured framework that outlines when decanting is permitted, the extent of permissible changes, and the safeguards designed to protect beneficiaries.

Many states have adopted the UTDA in full or in modified form, while others rely on their own statutes or common law principles. As a result, trustees must always confirm the governing law of the relevant jurisdiction before proceeding.

Trustee authority

A trustee’s power to decant can come from two sources.

- Express authority in the trust document: Some trusts explicitly grant the trustee the power to decant, often with specific conditions or limitations.

- State decanting statutes: In the absence of express language, state law may authorize decanting, provided certain statutory requirements are satisfied.

In all cases, trustees are bound by fiduciary duties and must exercise their authority in good faith, in accordance with the terms of the trust, and in the best interests of the beneficiaries.

State variations

Many states have enacted decanting statutes, while others rely on case law or require court approval. Rules can differ widely, including what changes are allowed, notice requirements, and whether the new trust can alter beneficiary rights.

Comparison of key states

| State | Decanting allowed? | Key feature |

|---|---|---|

Florida |

Yes |

Broad statutory framework with trustee discretion, subject to fiduciary duties. |

Texas |

Yes |

Detailed statutory provisions specifying limits and conditions. |

New York |

Yes |

Early adopter of their own decanting law; supported by statute and well-developed case law. |

California |

Yes |

Modern statutory framework with structured guidance for trustees. |

Delaware |

Yes |

Flexible statutes often used for advanced planning. |

Nevada |

Yes |

Extensive flexibility, frequently used in long-term and asset-protection trusts. |

South Dakota |

Yes |

Comprehensive statutory approach with modern trust laws. |

State law ultimately governs the decanting process, defines what changes are permissible, and ensures that trustees act within their legal and fiduciary boundaries. Before decanting, trustees should carefully review the applicable state law and seek qualified legal advice to ensure compliance and alignment with the trust’s objectives.

How state laws affect trust decanting: Current landscape

While the UTDA provides a model framework, not all states follow it uniformly. Some states adopted it fully, while others added their own restrictions, and still others rely on common law or court involvement. Below is a state-by-state breakdown of the current status of trust decanting.

States that have adopted the UTDA

The following states have passed laws based on the UTDA, offering a fairly consistent framework for trustees:

Alabama, California, Colorado, Connecticut, Illinois, Michigan, New Mexico, North Carolina, South Carolina, Virginia, West Virginia

In these states, trustees generally have clear statutory authority to decant if acting in the best interests of beneficiaries.

States with independent decanting statutes

Some states didn’t adopt the UTDA but did pass their own decanting laws, often with unique twists.

- Florida: Broad trustee discretion; very favorable to estate planners.

- Texas: Allows decanting but restricts changes to certain beneficiary rights.

- Nevada: Known for strong asset protection; generous to trustees.

- Delaware: Highly flexible, popular for trust planning.

- Alaska: A pioneer in modern trust decanting laws.

- New York: Another pioneer in modern trust decanting laws.

- South Dakota: One of the most favorable and flexible decanting statutes in the country.

- Washington: Washington state enacted a comprehensive decanting statute

- Arkansas: Arkansas enacted trust decanting legislation in 2023

- Arizona, Massachusetts, Missouri, New Jersey, Ohio, Tennessee, and Wisconsin: Each provides statutory authority, but with varying limits.

3. States without a specific decanting statute

In these states, trustees may still decant under common law or by seeking court approval, but the process is less predictable:

Georgia, Hawaii, Idaho, Indiana, Iowa, Kansas, Kentucky, Louisiana, Maine, Maryland, Minnesota, Mississippi, Montana, Nebraska, New Hampshire, North Dakota, Oklahoma, Oregon, Pennsylvania, Rhode Island, Utah, Vermont, Wyoming

Here, judicial involvement may be necessary, and the outcome depends on state precedent.

4. States restricting or silent on decanting

A small number of states either restrict decanting heavily or have not yet addressed it.

- Washington, D.C., recently passed decanting legislation narrower than UTDA.

- Some silent jurisdictions - Any states not mentioned above require case-by-case interpretation.

What is the step-by-step process for decanting a trust?

Decanting a trust is not simply rewriting the document. It is a formal legal process that must follow specific steps to ensure the trustee acts within their authority and protects the interests of beneficiaries. Below is a practical outline of how the process typically works.

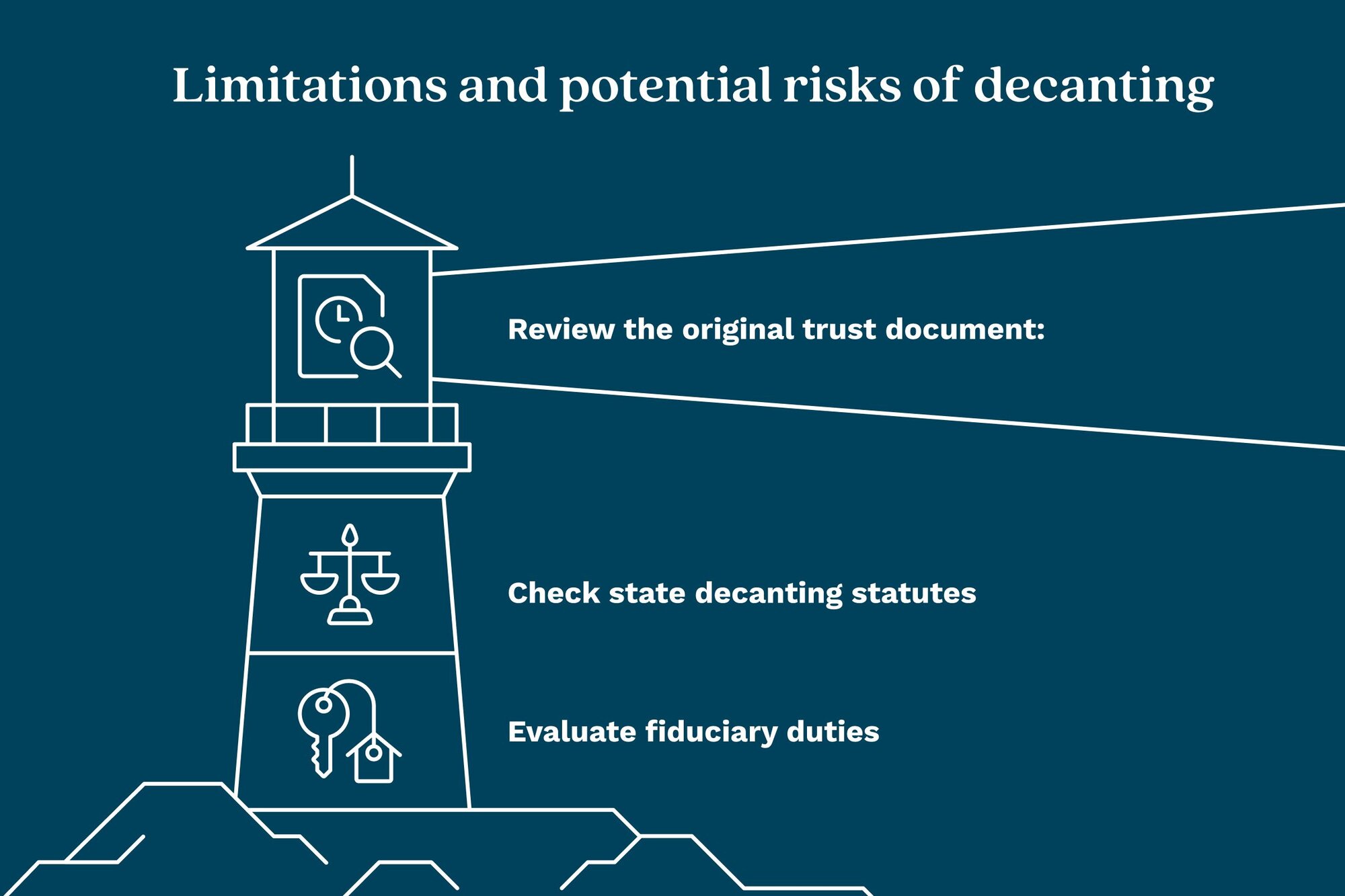

Step 1: Confirm whether state law permits decanting

The starting point is determining whether decanting is legally allowed. A trustee should:

- Review the original trust document. Start by carefully examining the trust instrument itself. Some trusts include an express decanting clause, which explicitly authorizes the trustee to move assets into a new trust. When such language exists, the process is often simpler because the trustee already has clear authority. If the trust is silent on decanting, further steps are required to confirm legal authority under state law.

- Check state decanting statutes. Even if the trust doesn’t explicitly allow decanting, many states have laws that grant trustees the power to decant. Most follow the Uniform Trust Decanting Act, while others rely on court decisions or may require judicial approval. Trustees should verify whether their state permits decanting and understand any restrictions or procedural requirements.

- Evaluate fiduciary duties. Regardless of statutory authority, the trustee must always act in accordance with fiduciary obligations. This includes exercising prudence, avoiding conflicts of interest, and acting in the best interests of all beneficiaries. Failure to meet fiduciary duties can expose the trustee to legal challenges or personal liability, even when decanting is otherwise allowed.

Step 2: Plan the new trust

Once confirmed that decanting is permitted, the trustee must create the new trust that will receive the transferred assets. This stage typically involves guidance from an experienced estate planning attorney to ensure the new document is properly drafted and legally sound while staying compliant with state law and the original trust’s intent.

Key issues to address when planning the new trust include:

- Distribution rules. Decide whether distributions should occur at different ages, under new conditions, or with added discretion for the trustee. The goal is to ensure distributions align with the beneficiaries’ current needs and the settlor’s intent.

- Asset protection. Consider strengthening spendthrift clauses or adding provisions to shield assets from creditors, divorcing spouses, or other risks.

- Special provisions. Determine whether the trust needs updates for special needs beneficiaries, digital assets, or modern administrative powers.

- Tax planning. Review the potential income, estate, and gift tax effects of the new trust to avoid creating unintended tax consequences.

A well-prepared drafting checklist for the new trust should cover:

- The scope of trustee powers and duties

- Updated distribution and management provisions

- Robust spendthrift and asset protection clauses

- Specific clauses for special needs or supplemental benefits (if applicable)

- Comprehensive tax allocation and reporting rules

Step 3: Provide beneficiary notice and observe waiting periods

Before any assets are moved, trustees generally have a legal obligation to notify beneficiaries about the proposed decanting. This step promotes transparency, gives beneficiaries an opportunity to understand and respond to the proposed changes, and helps minimize future disputes.

- Identify qualified beneficiaries. Begin by determining who must receive notice. “Qualified beneficiaries” generally include both current beneficiaries, who are entitled to receive income or principal, and remainder beneficiaries, who will receive assets after the trust term ends. It’s essential to accurately identify these individuals for compliance with state law.

- Prepare the notice. The notice should clearly communicate key information, including the trustee’s identity, a description of the proposed decanting, a copy or summary of the new trust, and an explanation of beneficiaries’ rights, such as the right to object or request additional information. Provide a clear, detailed notice to help maintain trust and avoid later challenges.

- Observe statutory waiting periods. Many states require that beneficiaries receive notice a specific number of days before the decanting can proceed, often between 30 and 60 days. Trustees must comply with these timelines to ensure the decanting is legally valid. When a trustee misses or ignores waiting periods, they can be exposed to legal challenges or disputes.

Step 4: Execute the transfer and retitle assets

After all notice requirements and waiting periods are met, the trustee can begin transferring assets from the original trust to the newly created trust. This stage focuses on ensuring that every asset is correctly retitled in the name of the new trust and that supporting documentation is complete and accurate.

- Retitle financial accounts. Update ownership for bank accounts, brokerage accounts, retirement accounts, and other investment holdings. Work closely with custodians or financial institutions to ensure all records accurately reflect the new trust.

- Record real estate transactions. For property owned by the old trust, execute new deeds and record them with the appropriate county or municipal office. Proper documentation ensures a clean transfer and helps avoid title disputes later.

- Handle unique or specialized assets. Assets such as business interests, closely held company shares, life insurance policies, or intellectual property may require additional consents, filings, or approvals before retitling. Trustees should coordinate with attorneys, insurers, or corporate officers to ensure compliance with all applicable laws and regulations.

- Maintain a detailed asset checklist. Keep a comprehensive record of every asset transferred, along with copies of deeds, account confirmations, and correspondence. A complete paper trail helps prevent errors, supports future audits, and protects the trustee from potential challenges.

Step 5: Finalize administration and recordkeeping

The final stage of the decanting process focuses on documentation and transparency. Proper record-keeping protects both the trustee and the beneficiaries, ensuring the new trust is legally sound.

- Update trust records. All changes made through decanting should be reflected in the trust’s official records. This includes amendments, updated terms, and details of asset transfers to the new trust.

- Record trustee decisions. Document the trustee’s actions and reasoning. Meeting minutes, formal resolutions, or written explanations should show that the decanting complied with applicable state laws and that the trustee considered the beneficiaries’ best interests.

- Communicate with beneficiaries. Keep beneficiaries informed at every stage. Open communication fosters trust, demonstrates good faith, and reduces the likelihood of disputes or confusion in the future.

- File or record public documents. If the decanting involves real estate or other assets requiring registration, file the appropriate deeds, titles, or public documents. Proper recording helps establish clear legal ownership and prevents future challenges.

- Maintain strong recordkeeping. Comprehensive, well-organized records support efficient trust administration and provide evidence that the trustee acted prudently in the event of questions or litigation.

Decanting is more than transferring assets; it is a deliberate, legally guided process that combines careful planning, adherence to state laws, and transparent communication with all parties involved.

Who has the authority to decant a trust?

A trustee can only decant a trust when the power comes from either the trust document itself or applicable state law. Any decanting must also be exercised within the trustee’s fiduciary duties. Trustees should confirm authority, follow proper procedures, and carefully document all decisions.

Express trust language vs. statutory authority

- Express decanting powers in the trust: Some trusts explicitly grant trustees the power to decant. When such language exists, the process is typically straightforward, because authority is clear.

- State law authority: If the trust is silent on decanting, trustees must rely on state statutes. Many states have decanting laws, often modeled on the Uniform Trust Decanting Act. Others depend on case law or require judicial approval.

- Governing law matters: Always determine which state law governs the trust. The trustee’s authority depends on the trust’s jurisdiction, and statutory rules may vary.

Scope and limits on trustee discretion

Trustees often have broad discretion under either the trust or state law. However, this discretion is not unlimited:

1. Trustees must act prudently, loyally, and in good faith.

2. The trustee’s decisions must serve the best interests of the beneficiaries.

3. Trustees should document the rationale for decanting to show that fiduciary duties were respected.

4. Trustees cannot:

- eliminate a beneficiary’s vested right to receive property,

- reduce a fixed income interest or mandatory distribution right,

- unreasonably increase their own trustee compensation or reduce their liability standard.

Common allowed scenarios for decanting

Trustees often dissent for practical, legitimate reasons.

- To fix outdated or invalid provisions, such as correcting ambiguous distribution language that creates administrative confusion.

- To update tax planning strategies, such as revising allocation language to reflect changes in estate or GST tax law.

- To change trustee succession, such as naming a corporate trustee or clarifying the process for appointing a successor.

Case examples (how decanting is used in practice)

- Special needs trusts. Decanting can add or clarify language that preserves a beneficiary’s eligibility for government benefits while allowing limited supplemental distributions.

- Spendthrift trusts. Decanting can reinforce or tighten spendthrift protections to limit creditor access to trust assets.

Who can challenge a decanting?

- Beneficiaries who believe the decanting harms their interests can sue.

- Creditors may challenge if the transfer frustrates legitimate claims.

- Other interested parties, such as guardians, conservators, or parties with standing under state law, may also object.

- Courts will review whether the trustee had authority and acted within fiduciary limits.

Practical checklist for trustees before decanting

- Confirm authority. Review the trust instrument for express decanting powers and check the governing state statute.

- Check the governing law. Confirm which state’s law applies to the trust and whether that state allows decanting.

- Assess conflicts of interest. Identify and address any personal or business conflicts before proceeding.

- Obtain legal and tax counsel. Get written advice outlining authority, tax consequences, and risks.

- Document the rationale. Prepare either trustee minutes or a written statement explaining why decanting serves the beneficiaries’ interests.

- Prepare proper notices. Draft and deliver statutory notices to qualified beneficiaries and observe any waiting periods.

- Consider court approval when the risk is high. If the changes are large, controversial, or cross state lines, consider seeking judicial guidance.

- Plan execution and recordkeeping. Map asset transfers, retitling steps, and retain copies of all documents and communications.

Limitations and potential risks of decanting

Decanting offers flexibility, but that flexibility is not unlimited. Trustees face legal, tax, and litigation risks if they overstep their authority or fail to follow proper procedures.

The “don’ts” of decanting a trust

Trustees must be mindful of boundaries. Decanting generally doesn’t allow:

- Additional beneficiaries. You can’t create an entirely new beneficiary class outside what the original trust allowed.

- Removal of vested rights. If a beneficiary is guaranteed mandatory distributions, those rights can’t usually be reduced or eliminated.

- Reduction of fiduciary accountability. Decanting can’t remove a trustee’s duty to act in good faith or weaken liability protections for beneficiaries.

- Alteration of the settlor’s core intent. The purpose the grantor had in creating the trust must remain intact.

Tax implications of decanting a trust

A poorly planned decanting can trigger significant tax issues. Key areas of concern include:

- Generation-skipping transfer (GST) tax. Moving assets into a new trust may affect the trust’s GST exemption.

- Income and capital gains tax treatment. Certain transfers can create unexpected income recognition events.

- State income tax considerations. If the trust’s governing law or location changes, the trust may face taxation in a new state.

Because of these risks, trustees should always coordinate with experienced tax counsel before decanting.

Litigation and trustee liability risks

Even when legally permitted, decanting often creates friction between beneficiaries. Risks include:

- Beneficiary disputes. Those who feel disadvantaged by the new trust terms may challenge the decanting in court.

- Procedural flaws. Failing to give proper notice or observe statutory waiting periods can render the decanting invalid.

- Trustee liability. Trustees may be held personally liable if they act outside their authority or fail to document their decision-making process.

How to reduce litigation risk

- Obtain legal counsel. Independent fiduciary or estate-planning advice shows good faith.

- Document thoroughly. Keep written minutes, trustee resolutions, and legal opinions to support the decision.

- Communicate with beneficiaries. Clear notice and open dialogue often prevent disputes before they escalate.

- Consider court approval. In controversial situations, judicial oversight can provide protection against later claims.

The bottom line: The risks of trust decanting must be managed carefully. Trustees should never proceed without a full understanding of the legal, tax, and fiduciary boundaries.

Alternatives to decanting a trust

Decanting is only one way to update or fix a trust. Depending on the trust’s terms, state law, and beneficiary cooperation, alternatives may be more suitable or safer.

Judicial modification (court approval)

A trustee or beneficiary can petition the court to modify a trust. Courts may approve changes if circumstances have changed in ways not anticipated by the settlor.

- Pros: Legally secure, court-supervised, minimizes trustee liability

- Cons: Costly, time-consuming, public (less privacy)

Trust merger or termination

When two trusts with similar terms and beneficiaries combine (or merge) into one trust. If the trust’s assets are small or administration is impractical, termination may be allowed under state law.

- Pros: Simplifies administration and cuts costs

- Cons: Limited situations; cannot be used simply to “rewrite” trust terms

Nonjudicial settlement agreement (NJSA)

An NJSA is a private agreement among the trustee and all qualified beneficiaries to resolve trust matters. These are commonly used to interpret ambiguous provisions, approve trustee actions, or make administrative changes. There are state law limits on when this approach can be used, so it’s important to work with an attorney.

- Pros: Faster, cheaper, avoids court

- Cons: Requires consent of all beneficiaries (sometimes impossible in large or conflicted families)

Limitations: A nonjudicial settlement agreement cannot violate a material purpose of the trust.

Trust protector provisions

A trust protector is a third party named in the trust with powers to amend or adjust certain terms. This could include modifying administrative provisions, updating tax references, or even replacing trustees.

- Pros: Built-in flexibility without court or statutory decanting

- Cons: Limited by the scope of powers granted in the trust

Important: This option only exists if the original trust document gives the protector authority.

Decanting vs. alternatives—when to choose each

- Decanting: Best for restructuring long-term trusts where flexibility is needed without going to court

- Judicial modification: Safer when beneficiary rights are being altered, or when the decanting authority is unclear

- NJSA: Works well for administrative fixes with unanimous beneficiary consent

- Trust protector: Useful if the settlor foresaw the need for future adjustments

- Merger/termination: Suitable for streamlining or winding down smaller, duplicative trusts

The bottom line: Trustees should weigh decanting vs trust modification carefully.

Real-world examples and use cases of trust decanting

Decanting is often used to modernize old trusts, protect beneficiaries, or respond to legal changes. Below are common scenarios and anonymous case studies that show both successes and cautionary lessons.

Common use cases

- Tax law compliance: Update trusts to reflect new estate tax exemptions or GST rules.

- Special needs planning: Preserve government benefits for a disabled child by restructuring distributions.

- Outdated distribution terms: Extend or modify mandatory payout ages to prevent wasteful spending.

- Asset protection: Move assets into a trust governed by a state with stronger creditor protection.

Case study 1: Updating for tax law changes

- Before: A 1990s trust required mandatory distributions, triggering unintended estate tax inclusion.

- Action: Trustee decanted into a new trust with flexible distribution standards and GST allocation language.

- Outcome: Reduced potential estate tax liability and aligned the trust with modern tax planning strategies.

- Lesson: Decanting can “future-proof” trusts against evolving tax codes.

Case study 2: Protecting a child with special needs

- Before: The original trust gave outright distributions at age 25. The child later developed a disability and qualified for government assistance.

- Action: Trustee decanted into a new special needs trust that restricted distributions to preserve eligibility.

- Outcome: Beneficiary retained public benefits while still receiving supplemental support from the trust.

- Lesson: Decanting can pivot an outdated trust into a tool for long-term care and stability.

Case study 3: Eliminating outdated mandatory distributions

- Before: A trust required lump-sum distributions at age 30. The trustee worried a spendthrift beneficiary would squander assets.

- Action: Trustee decanted into a discretionary trust with staggered distributions at 30, 35, and 40.

- Outcome: Assets remained protected, and distributions were better aligned with the beneficiary’s maturity and needs.

- Lesson: Decanting can be used to add guardrails when the original terms no longer fit real-world circumstances.

Cautionary example: When decanting failed

- Scenario: A trustee attempted to decant in order to cut out a beneficiary with vested rights. The beneficiary sued, claiming breach of fiduciary duty.

- Court outcome: The court voided the decanting, reinstated the beneficiary’s rights, and held the trustee personally liable for legal costs.

- Lesson: Trustees must respect statutory and fiduciary limits—decanting is not a shortcut to disinheriting or overriding vested rights.

Takeaway: Real-world decanting outcomes range from powerful success stories to cautionary missteps. The key is aligning the process with state law, fiduciary duty, and the settlor’s intent.

Can LegalZoom help you decant your trust?

Decanting rules differ by state and can impact taxes, distributions, and beneficiary rights. LegalZoom can connect you with experienced estate planning attorneys in all 50 states by accessing a legal plan that allows for unlimited consultations on new legal topics.

FAQs about decanting trusts

How long does the decanting process take?

The timeline varies depending on the state’s notice requirements, the type of assets in the trust, and the complexity of the changes. In states with a statutory notice period, the process can take anywhere from 30 to 90 days. More complex trusts involving multiple beneficiaries or real estate may take several months, especially if court involvement is required.

Does the new decanted trust get a new Tax ID Number (TIN)?

In many cases, yes, especially if the trust’s tax status changes or if the IRS views the new trust as a separate legal entity. However, some decantings may preserve the original TIN if the IRS rules that the trust is simply a continuation. Always confirm with a tax professional before making changes.

How much does it cost to decant a trust?

Costs depend heavily on the trust’s complexity, state law requirements, and professional fees. Simple decantings may cost a few thousand dollars in legal work, while complex cases with court involvement, multiple assets, or tax planning considerations may cost $10,000 or more. Legal fees, trustee fees, and filing costs should all be factored in.

What are common red flags that should trigger court involvement?

Court approval may be necessary if the proposed decanting:

- Alters beneficiary classes or eliminates vested rights

- Involves conflicting beneficiary interests

- Raises disputes about the trustee’s authority

- Creates significant tax implications or changes the trust’s status

When in doubt, trustees should seek judicial confirmation to reduce liability risk.

Is decanting the same as creating a new trust?

Not exactly. Decanting transfers assets into a new trust, but the original trust still exists for historical and legal purposes.

Can beneficiaries stop or object to a trust decanting?

Yes, beneficiaries can challenge in court if they believe their rights are harmed or that proper notice wasn’t given.

Does trust decanting affect Medicaid or special needs planning?

Yes, one of the main uses is to preserve government benefit eligibility by updating the trust terms.

Can you decant a trust more than once?

Oftentimes, you can, as long as the trustee retains authority under statute or the trust document. Some states place limits, so make sure you have talked to an estate professional.

Is decanting always better than modifying a trust?

No, decanting is not always the best option. There are other options, but you should consult an attorney to determine what is best for your specific circumstances.

'%20/%3e%3c/svg%3e)

'%3e%3cpath%20fill-rule='evenodd'%20clip-rule='evenodd'%20d='M9.31239%2025.5316H13.0679V14.1032H9.31239V25.5316ZM11.1913%208.46875C9.93945%208.46875%209%209.25086%209%2010.505C9%2011.5995%209.78211%2012.5389%2011.1913%2012.5389C12.6005%2012.5389%2013.3826%2011.5995%2013.3826%2010.505C13.3826%209.4082%2012.6005%208.46875%2011.1913%208.46875ZM27%2018.9577V25.5316H23.2445V19.4275C23.2445%2017.8609%2022.6174%2016.7664%2021.3679%2016.7664C20.2711%2016.7664%2019.644%2017.5463%2019.3316%2018.1756C19.1743%2018.488%2019.1743%2018.8004%2019.1743%2019.1128V25.5316H15.4165V13.9458H19.1743V15.5123C19.644%2014.7302%2020.5835%2013.6357%2022.6174%2013.6357C25.1234%2013.7908%2027%2015.3573%2027%2018.9577Z'%20fill='white'/%3e%3c/g%3e%3cdefs%3e%3cclipPath%20id='clip0_952_9489'%3e%3crect%20width='18'%20height='18'%20fill='white'%20transform='translate(9%208)'/%3e%3c/clipPath%3e%3c/defs%3e%3c/svg%3e)